Introduction

Insurance operations run on paper (or the digital equivalent). Every day, adjusters receive claims packets combining scanned PDFs, mobile-uploaded damage photos, handwritten accident reports, emailed loss narratives, and faxed medical bills. No two look alike, and no two arrive through the same channel.

The operational cost is real. According to Accenture research covering 434 US underwriters, the average underwriter spends 40% of working time on administrative tasks — time that should go toward actual risk assessment. Multiply that across a claims team during a catastrophe event (Verisk recorded approximately 350,000 excess claims for Hurricane Helene within 75 days), and manual intake queues become a serious liability.

Intelligent document processing (IDP) addresses this directly — but how it works remains poorly understood. Insurers implement it expecting immediate results and get misaligned outcomes because the pipeline underneath is never explained clearly.

This guide breaks down exactly how IDP works in insurance, stage by stage, so you can assess it accurately, deploy it effectively, and avoid the implementation pitfalls that derail most projects.

Key Takeaways

- IDP combines OCR, NLP, computer vision, and ML to capture, classify, extract, validate, and route insurance document data automatically

- Unlike basic OCR, IDP understands document context — handling unstructured, semi-structured, and structured formats without separate templates for each

- Four sequential stages power the pipeline: ingestion, extraction and classification, validation, and system integration

- Core insurance workflows transformed include claims/FNOL, underwriting, fraud detection, and policy administration

- When implemented correctly, STP enables touchless processing for routine claims — cutting cycle times from days to minutes

What Is Intelligent Document Processing?

IDP is a technology stack (not a single tool) that combines OCR, NLP, machine learning, and computer vision to automatically ingest, classify, extract, and validate data from documents. Traditional OCR reads text. IDP understands it — classifying documents, resolving ambiguity, and routing data into downstream systems without manual intervention.

That distinction matters because the industry produces enormous document volumes from radically different sources. A single claims packet can arrive as a fax, a mobile photo, an email attachment, and a web portal upload — simultaneously. No two broker submissions share the same layout. Rules-based OCR and RPA break the moment a form changes format.

What IDP Is Not

A few important clarifications before going further:

- Not a bolt-on OCR upgrade — IDP is a coordinated pipeline of cooperating technologies

- Not fully autonomous — human-in-the-loop review for exceptions is a deliberate design feature, not a limitation

- Not template-dependent — a trained IDP system handles new document layouts without manual reconfiguration

The Three Document Types IDP Handles

| Document Type | Insurance Examples | Processing Challenge |

|---|---|---|

| Structured | CMS-1500 medical claims, standardized FNOL forms | Consistent fields, but volume and format variations |

| Semi-structured | Invoices, repair estimates, broker submissions | Variable layouts, inconsistent field placement |

| Unstructured | Adjuster emails, handwritten accident reports, loss narratives | No fixed format, free-form language |

The processing path through the IDP pipeline differs slightly for each type — but a well-built system handles all three without requiring separate templates.

How IDP Works in Insurance: The Four-Stage Pipeline

IDP runs as a defined sequence — each stage transforms the document before passing it to the next. Knowing what happens at each stage is what allows insurers to deploy it effectively rather than expensively.

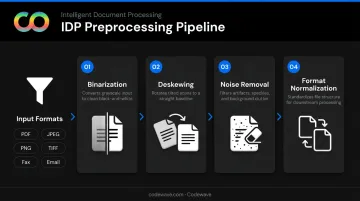

Stage 1: Document Ingestion and Preprocessing

Before any text is read, the document needs to be made readable.

IDP ingests from all input channels simultaneously — email attachments, scanned PDFs, mobile photo uploads, fax-to-digital feeds, and web portals — without requiring a standardized input format. AWS's insurance-specific IDP architecture documents intake from fax, email, and administrative portals, with PDF, Word, plain-text, JPEG, PNG, and TIFF all supported.

Once ingested, preprocessing runs automatically:

- Binarization — converts grayscale scans to clean black-and-white for OCR readability

- Deskewing — corrects tilted images from uneven scanning or hand-held phone shots

- Noise removal — eliminates artifacts, stray marks, and compression distortion

- Format normalization — standardizes file types for consistent downstream processing

The common bottleneck here isn't the technology — it's input quality. Poor scan quality, mixed-format packets (one claim arriving as a PDF, a JPEG, and a handwritten supplement), and catastrophe-event volume spikes all stress intake queues.

Systems that handle preprocessing well absorb these spikes. Ones that don't create the backlogs that frustrated adjusters already know.

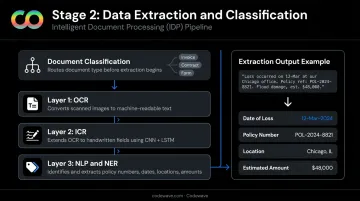

Stage 2: Data Extraction and Classification

This is where IDP's intelligence separates it from basic OCR.

Classification comes first. AI models identify the document type before any extraction begins — distinguishing a police report from a medical bill from a policy endorsement. This allows one IDP system to handle dozens of document types without a separate template for each. Codewave builds these classification layers using BERT or RoBERTa models fine-tuned on client-specific document sets, enabling automatic routing: claim forms go to claims processing queues, contracts route to compliance engines.

Extraction runs in parallel layers:

- OCR converts scanned images and image-only PDFs into machine-readable text

- ICR (Intelligent Character Recognition) extends OCR to handwritten fields — common in accident reports and hand-filled claim forms — using CNN + LSTM model architectures that learn sequential handwriting patterns

- NLP and Named Entity Recognition (NER) process the extracted text to identify and tag specific entities

NER pulls structured data from unstructured language — the step that turns raw extracted text into fields a claims system can actually use.

A concrete example: From a plain-text email reading "The incident occurred on June 14 under policy AF12987 at the Riverside location," NER extracts:

- Date of Loss:

2025-06-14 - Policy Number:

AF12987 - Location:

Riverside

AWS's insurance NER implementation identifies entities including policy holder name, beneficiary name, policy number, payout amounts, and required actions. For health claims, it maps medical text to ICD-10-CM, RxNorm, and SNOMED CT codes and flags PHI for HIPAA-compliant redaction.

Before data moves downstream, normalization runs on dates, address formats, and monetary values — "Nov 1, 2025" becomes 2025-11-01, ensuring compatibility with whatever claims management system receives the output.

Stage 3: Validation and Anomaly Detection

Extracted data doesn't flow directly into systems. It gets verified first.

The validation layer cross-references extracted data against:

- Existing policy records and coverage terms

- External databases (DMV records, medical provider registries, property data)

- Regulatory requirements and business rules

A claimant address that doesn't match the policy record, a date of loss outside the policy period, or a repair estimate that exceeds vehicle value — all trigger automatic flagging for human review. This catches transcription errors and data conflicts before they contaminate downstream systems.

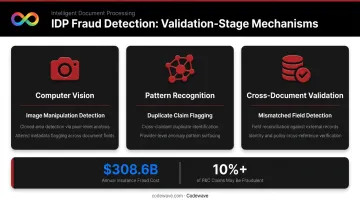

Fraud detection runs at this same stage, and it operates differently from simple rule-checking. Deloitte's 2025 insurance fraud analysis identifies ML-powered anomaly detection, network-link analysis, and text mining as the core fraud detection mechanisms — not rules alone. In practice, this means:

- Computer vision scans images for manipulation — cloned damage areas, altered metadata, inconsistent lighting suggesting photo editing

- Pattern recognition flags duplicate claim patterns across claimants, providers, or vehicles

- Cross-document validation catches mismatched fields between submitted documents and external records

The scale justifies the investment. The Coalition Against Insurance Fraud estimates fraud costs American consumers at least $308.6 billion annually, with industry estimates suggesting 10% or more of P&C claims may be fraudulent. Manual fraud review at that volume isn't a viable strategy.

Stage 4: System Integration and Output

The pipeline's final stage pushes validated, structured data directly into downstream platforms — no manual re-entry.

Modern IDP connects to claims management systems (Guidewire ClaimCenter via Cloud APIs and Integration Gateway), policy administration systems (Duck Creek via Integration Fabric, SAP via OData Insurance Claim Service), and CRM tools through REST APIs and pre-built connectors. For legacy systems without modern API support, RPA bots handle the handoff.

What happens to exceptions: Documents that fail validation or fall below confidence thresholds don't get discarded — they route to a human review queue with flagged fields highlighted. Adjusters see exactly which data point triggered the flag and why, making review faster than working through the original document manually.

This is where straight-through processing (STP) becomes possible. When a complete, consistent claims packet clears all four stages — ingested cleanly, classified correctly, extracted accurately, validated without conflicts — it moves from intake to resolution without any human touchpoint. For high-volume insurers, that translates to measurable cycle time reductions and a lower cost per claim — both at scale.

Where IDP Makes an Impact Across Insurance Operations

IDP applies across the full insurance lifecycle, but the mechanics differ by workflow.

Claims and FNOL

FNOL is typically where insurers start IDP implementations — and for good reason. Multi-format submissions arrive in bulk, especially after weather events, and manual intake creates backlogs measured in days. IDP reads submissions across formats, classifies document types, extracts loss details, and pre-populates claims management systems within minutes of receipt.

Underwriting

Underwriters already spend roughly 40% of their time on administrative tasks — pulling data from financial statements, inspection reports, and broker submissions before any actual risk judgment happens. IDP extracts those attributes directly and feeds rating models, returning that capacity to the work only underwriters can do.

Policy Administration

Policy issuance stalls when documents are missing or KYC re-validation sits in a queue. IDP handles that automatically:

- Flags incomplete application packets before they reach underwriting

- Re-validates KYC data during renewals without manual review

- Triggers e-signature workflows at the right stage in the process

Fraud and Compliance

Beyond individual claim validation, IDP creates tamper-proof audit trails with automatic logging and timestamping on every processed document. This supports HIPAA and GDPR compliance requirements and enables consistent cross-document fraud screening across thousands of claims simultaneously.

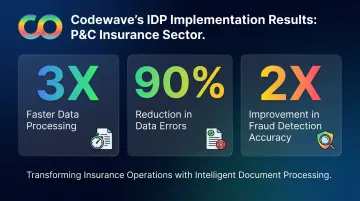

For P&C insurance clients, Codewave's IDP implementations have delivered 3X faster data processing, 90% fewer data errors, and a 2X improvement in fraud detection accuracy — results that follow when each pipeline stage is built for the specific document types and workflows involved.

Conclusion

IDP's value lies in the sequence — ingestion, classification, extraction, validation, and integration — with each stage eliminating a specific failure point that manual processing consistently produces.

Insurers who understand the pipeline make better decisions. They know where to start — FNOL and claims intake are the right entry points — which metrics matter (cycle time, error rate, and STP percentage), and what to expect from each implementation phase.

If you're evaluating IDP for a specific workflow or looking to recover value from an existing implementation that isn't performing, Codewave designs and builds these systems for insurance clients — prioritizing the workflows where manual processing carries the highest cost. Explore how Codewave approaches IDP implementation for insurance operations.

Frequently Asked Questions

What is the difference between IDP and OCR in insurance?

OCR converts document images to machine-readable text but has no understanding of meaning or context. IDP layers NLP, ML, and validation logic on top of OCR output to classify documents, extract named entities, and validate data against business rules. That combination is what allows IDP to handle the unstructured, variable formats that OCR alone consistently fails on.

What types of insurance documents can IDP process?

A well-trained IDP system handles all three major document categories without requiring separate templates for each:

- Structured forms: CMS-1500 medical claims, standardized FNOL forms

- Semi-structured documents: invoices, repair estimates, broker submissions

- Unstructured content: adjuster emails, handwritten accident reports, free-form loss narratives

How does IDP help detect insurance fraud?

IDP applies fraud detection at intake speed across three mechanisms:

- Image analysis: ML-powered computer vision identifies manipulation such as cloned damage areas or altered metadata

- Cross-validation: submitted data is checked against policy records and external databases

- Anomaly flagging: mismatched fields and duplicate claim patterns trigger automated review

Every document passes through the same fraud screen, with no gaps from manual fatigue or inconsistent review.

Can IDP integrate with existing insurance core systems?

Yes. Modern IDP connects to the most common insurance core platforms:

- Guidewire ClaimCenter: via Cloud APIs and Integration Gateway

- Duck Creek: via Integration Fabric

- SAP: via OData services

For legacy systems without API support, RPA bots bridge IDP outputs without requiring platform replacement.

What is straight-through processing and how does IDP enable it?

STP is the ability to move a claim from receipt to resolution without manual intervention. IDP enables it by ensuring extracted data is complete, validated, and correctly formatted before reaching downstream systems. Routine, clean claims then require no human touchpoint at any stage.

How long does it take to implement IDP in an insurance company?

Timelines depend on document complexity, integration requirements, and training data availability. Focused implementations starting with a single high-volume workflow like FNOL intake typically go live in weeks. Broader rollout expands as the system is trained on additional document types and connected to more downstream systems.