For insurance operations managers, claims team leads, and IT decision-makers, this matters for a direct reason: manual claims handling introduces delays, errors, compliance risk, and inflated costs that erode both customer trust and profitability. According to McKinsey, improved claims management can reduce loss adjustment expenses by 25–30% and total claims costs by 6–7%.

This guide explains how automated claim processing works end-to-end, what technologies make it effective, and where teams commonly go wrong when applying it.

Key Takeaways

- Automated claim processing uses AI, RPA, OCR, and NLP to reduce manual effort and errors across the full claims lifecycle

- Claims move through intake → extraction → validation → adjudication → settlement, with human escalation for complex cases

- Fraud screening runs in parallel — roughly 10% of P&C losses involve fraud, making this step non-optional

- Success hinges on data quality, legacy system integration, and defining which claim types to automate

- Full automation is not universally appropriate — complex, ambiguous, or disputed claims still require human judgment

What Is Automated Claim Processing?

Automated claim processing applies intelligent technologies — AI, ML, RPA, OCR, and NLP — to digitize, route, and resolve insurance claims with reduced human intervention in repetitive, rule-based work.

The goal goes beyond digitizing paperwork. Done right, it produces faster, more consistent claim decisions that lower cost-per-claim and improve policyholder experience at scale.

A few distinctions matter here:

- A digital claims portal handles intake only — capturing submissions without automating the decisions that follow

- Most implementations sit between partial automation (data extraction only) and straight-through processing (end-to-end resolution with no human touch for eligible claims) — full AI decision-making is one edge of that range, not the norm

- The most effective deployments pair automated pipelines for well-defined claim types with structured escalation paths for edge cases and exceptions

Why Insurance Teams Use Automated Claim Processing

The Operational Pressures Driving Adoption

Manual claims handling creates compounding problems: high volumes of repetitive data entry, long cycle times, re-work from transcription errors, and inconsistent adjudication decisions across adjusters. At scale, these inefficiencies compound fast — and automation is how leading insurers are getting ahead of them.

What insurance operations specifically need from automation:

- Consistency — uniform application of coverage rules regardless of which adjuster handles the file

- Audit-ready documentation — every action logged automatically for regulatory review

- Surge capacity — the ability to handle catastrophic loss events without proportionally scaling headcount

- Real-time policyholder communication — status updates that don't require a staff member to send

The Adoption Landscape

The gap between intent and execution is real. Accenture found that 79% of claims executives believe AI and automation can add value across the claims value chain — but only 35% describe their organizations as advanced in using these technologies. Yet 65% planned to invest $10M or more in AI-based applications over the next three years — signaling that the gap between intent and execution is closing.

That investment is driven by two converging forces. Insurers across P&C, health, and life lines face regulatory reporting expectations that manual processes struggle to meet consistently — and policyholders now benchmark their claims experience against the same consumer-grade digital interactions they get from retail and banking apps.

What Goes Wrong Without Automation

- Delayed settlements trigger regulatory scrutiny under prompt-payment rules

- Inconsistent adjudication creates dispute exposure and appeals overhead

- Manual fraud review misses patterns that ML models detect across thousands of claims simultaneously

- Lack of real-time status updates drives inbound call volume and erodes customer satisfaction

How Automated Claim Processing Works

Claims enter through one or more intake channels, where automated tools extract, structure, and validate the data against policy records. From there, the claim either resolves through straight-through processing or routes to a human adjuster with context already pre-populated. Every action throughout this flow is logged for compliance and audit purposes.

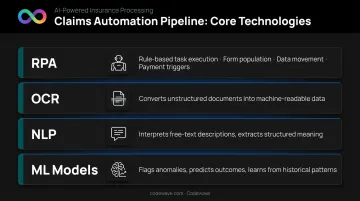

The core technologies powering each stage:

| Technology | Role in the Claims Pipeline |

|---|---|

| RPA | Rule-based task execution — form population, data movement, payment triggers |

| OCR | Converts unstructured documents (receipts, medical reports, photos) into machine-readable data |

| NLP | Interprets free-text claim descriptions and extracts structured meaning |

| ML models | Flags anomalies, predicts claim outcomes, improves from historical patterns |

Codewave implements this stack for insurance teams using Google Cloud Vision API, ABBYY FineReader, and Tesseract for document processing, alongside transformer-based classification models that route claim forms to the correct processing queue automatically.

Step 1: First Notice of Loss (FNOL) and Digital Intake

The process starts when a policyholder submits a claim through a digital channel — web portal, mobile app, email, or API integration. Automation captures the claim details, timestamps the event, and initiates the workflow without requiring a staff member to touch it.

FNOL automation delivers two concrete improvements:

- Faster acknowledgment — policyholders receive immediate confirmation rather than waiting for business hours

- Cleaner data — transcription errors from manual phone intake or paper forms are eliminated at the source

Step 2: Data Extraction, Validation, and Fraud Screening

Once submitted, OCR and NLP tools extract relevant data from attached documents — photos, invoices, medical records, police reports — and structure it into the claims management system. The system then cross-checks extracted data against the policyholder's coverage limits, deductibles, and claim history.

ML-based fraud detection runs in parallel. Algorithms analyze the claim against historical patterns to flag anomalies: duplicate billing codes, implausible incident timelines, unusual provider billing patterns. Suspicious claims route to a special investigative unit rather than processing automatically.

The Coalition Against Insurance Fraud estimates that fraud occurs in roughly 10% of property-casualty insurance losses, costing U.S. consumers at least $308.6B annually. Manual review cannot catch patterns at that scale consistently.

Step 3: Adjudication, Decision, and Settlement

Predefined rules and coverage logic determine whether a claim qualifies for straight-through processing or requires human adjuster review:

- Simple, low-complexity claims — auto-approved, payment initiated, settlement notice generated, claim record closed with full audit trail

- Flagged or high-value claims — escalated to an adjuster with all relevant information pre-populated, reducing review time rather than eliminating the human

For eligible claims, this compresses settlement timelines from days or weeks to hours. McKinsey has projected that by 2030, more than half of claims activities could be replaced by automation, with resolution turnaround for many claims measured in minutes rather than days.

Key Factors That Affect Automated Claim Processing

Not every insurance operation will see the same results from automation. These five factors determine whether an implementation performs or underperforms:

Data quality and completeness — ML models perform only as well as the historical claims data they train on. Inconsistent, incomplete, or biased data degrades extraction accuracy and fraud detection reliability. This is the most common underestimated risk.

Legacy system integration — many insurers rely on older policy administration and billing systems that require custom middleware or API layers to connect with modern automation platforms. McKinsey notes that proprietary core system builds can take five to ten years, while commercial platforms typically require three to five — plan integration timelines accordingly.

Claim type and complexity — structured, high-volume, low-ambiguity claims (auto glass, straightforward property damage) are well-suited for automation. Unstructured, multi-party, or high-dispute claims reduce automation effectiveness significantly.

Regulatory and compliance constraints — automation must account for jurisdiction-specific handling rules, required response windows, and data privacy laws. The NAIC's Model Bulletin on AI Systems (December 2023) covers claim administration and fraud detection — 25 states had adopted related guidance by April 2026. Health claims add HIPAA obligations for any vendor touching protected health information.

Volume and scalability requirements — automation ROI is most evident at scale. Teams processing low claim volumes may not justify full implementation; high-volume operations benefit most from straight-through processing rates.

Common Issues and Misconceptions

Automation Does Not Mean Removing Humans

Many teams assume deploying claims automation means eliminating human involvement. Effective implementations define clear escalation thresholds so humans handle cases that require genuine judgment, rather than spending time on repetitive data entry.

The Cigna PXDX case illustrates what happens without this distinction. ProPublica reported that Cigna medical directors used the system to deny more than 300,000 claims over two months, averaging 1.2 seconds of review per case. The result was regulatory scrutiny and class action litigation — not operational efficiency.

"Set and Forget" Degrades Performance

Claims automation requires ongoing model retraining, rule updates as policy products change, and exception monitoring. Teams that configure automation once and leave it see two outcomes: degrading accuracy over time and increasing false-positive escalation rates that force more manual review, not less.

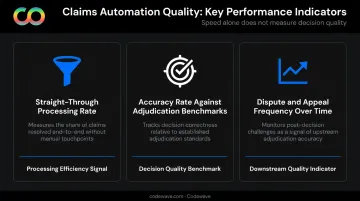

Speed Is Not a Proxy for Accuracy

A claim processed quickly through an automated pipeline is not automatically a correctly adjudicated claim — speed measures the process, not the decision quality. Insurance teams should track a fuller picture:

- Straight-through processing rates

- Accuracy rates against adjudication benchmarks

- Dispute and appeal frequencies over time

Speed is one data point. The others tell you whether your automation is actually working.

When Automated Claim Processing May Not Be Appropriate

Automation is a tool, not a default. These are the situations where applying it creates more problems than it solves:

Claim types where automation is counterproductive:

- Complex multi-party liability claims

- Claims involving subjective injury assessments (chronic pain, mental health conditions)

- Large commercial losses requiring negotiation

- Any claim where policy interpretation is genuinely ambiguous

Organizational constraints that reduce effectiveness:

- Severely fragmented or poor-quality historical claims data that cannot support reliable ML model performance

- Frequent product changes that create high rule-maintenance overhead, offsetting processing efficiency gains

- Understaffed adjuster teams without capacity to review, correct, or retrain automated decisions — leaving errors undetected

When those constraints go unaddressed, they show up as measurable failure patterns. Signals that automation is being misapplied:

If any of these are true, recalibrate the configuration before expanding coverage:

- Exception escalation rates exceed straight-through processing rates

- Adjuster override of automated decisions is frequent

- Fraud flagging produces high false-positive rates that consume investigative capacity without generating proportional catches

Each of these signals points to a configuration problem, not a fundamental flaw in the approach. The fix is recalibrating the claims population the system is built around, not abandoning automation altogether.

Conclusion

Automated claim processing accelerates the claims lifecycle by handling intake, data extraction, validation, fraud screening, and settlement through integrated AI and automation tools — freeing adjusters for complex cases that require human judgment, negotiation, or policy interpretation.

The real payoff comes from deploying automation precisely — matching the right automation depth to the right claim types, maintaining data quality, and preserving meaningful human oversight at the right points in the workflow.

For insurance teams evaluating or scaling claims automation, an experienced technology partner accelerates time-to-value. Codewave has built AI-powered automation solutions across insurance and financial services, with documented outcomes including 99% reduced fraud risk and 50% faster processing. Engagements follow an outcome-based model — results are defined and tracked from day one.

Frequently Asked Questions

What is automated claims processing?

Automated claims processing uses AI, RPA, OCR, NLP, and machine learning to manage the claims lifecycle — from intake and data extraction through validation, adjudication, and settlement — with minimal manual intervention, delivering faster, more consistent decisions at lower cost per claim.

What are the steps in claims processing?

The core steps are: FNOL/claim intake, data extraction and document review, validation and fraud screening, adjudication and decision-making, and payment/settlement. Automation can be applied at each stage to varying degrees depending on claim complexity and organizational data readiness.

What is RPA in insurance?

Robotic Process Automation (RPA) in insurance refers to software bots that execute rule-based, repetitive tasks — extracting claim data from forms, moving files between systems, and triggering payment workflows — without human intervention. RPA serves as the execution layer within a broader claims automation stack.

How does automation help detect insurance fraud?

ML models analyze incoming claims against historical data to flag anomalies (duplicate billing codes, unusual provider patterns, implausible incident details) and automatically route suspicious cases to investigators rather than straight-through settlement — catching pattern-based fraud that manual review misses at volume.

Can automation fully replace human claims adjusters?

No. Automation handles well-defined, high-volume, low-complexity claims efficiently but cannot replace human judgment for complex, ambiguous, or high-dispute cases. Effective implementations define clear escalation rules so adjusters focus on cases requiring negotiation, empathy, or genuine policy interpretation.

What are the biggest challenges of implementing claims automation?

The four most common obstacles are legacy system integration, data quality gaps that limit AI model accuracy, compliance with jurisdiction-specific regulations (NAIC AI guidelines, HIPAA), and employee adoption. Structured change management and reskilling programs are critical to addressing that last point.