The numbers reflect how seriously the industry is taking this. According to Deloitte's 2025 research covering 200 US insurance executives, 76% have already implemented generative AI in at least one business function — yet only 25% of insurer transformation programs are rated highly successful. Adoption is accelerating; execution is the gap.

This article covers what intelligent automation actually means in an insurance context, which use cases generate the clearest ROI, what business benefits operators are realizing, and how to build a practical implementation path that avoids the most common failure points.

Key Takeaways

- Combining AI, ML, and NLP with RPA lets insurers automate both high-volume routine tasks and judgment-intensive workflows — not just one or the other

- Claims processing and underwriting deliver the highest-impact ROI, with documented drops in turnaround time and operational cost

- ML-based fraud detection flags suspicious claims in real time — critical when insurance fraud costs the industry an estimated $308.6B annually

- Automation quality directly shapes customer retention; poor digital claim experiences are a leading driver of policyholder churn

- Start with high-volume, high-error workflows; connect your data before deploying bots

What Is Intelligent Automation in Insurance?

Traditional RPA follows a script. It copies data between systems, fills forms, and triggers predefined actions. Fast and reliable — but only within the exact rules it was given. Feed it an unstructured document or an edge case, and it stops cold.

Intelligent automation (IA) layers AI, machine learning, and NLP on top of that RPA foundation — giving the system the ability to handle unstructured data, recognize context, and improve its own accuracy over time. Where RPA executes, IA interprets first.

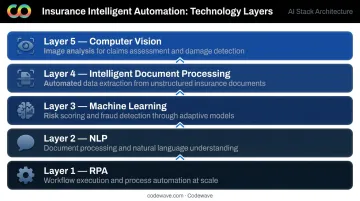

The Core Technology Stack

In insurance, a full IA stack typically includes:

- RPA — workflow execution, system-to-system data movement, automated correspondence

- NLP — processing policies, claims narratives, emails, and legal documents

- Machine learning — risk scoring, fraud pattern detection, predictive modeling

- Intelligent document processing (IDP) — extracting structured data from medical records, damage photos, and handwritten forms

- Computer vision — analyzing images for damage assessment or fraud inconsistencies

Why Insurance Fits IA So Well

Insurance is document-heavy, data-intensive, regulatory-sensitive, and dependent on fast, accurate decisions at scale. Underwriters spend roughly 40% of their time on non-core activities, according to Accenture — not risk assessment, but data gathering, form handling, and administrative work. That's exactly the gap IA fills.

Key Use Cases of Intelligent Automation in Insurance

Claims Processing Automation

Claims is where most insurers feel operational pain most acutely — and where IA delivers its fastest, most measurable impact.

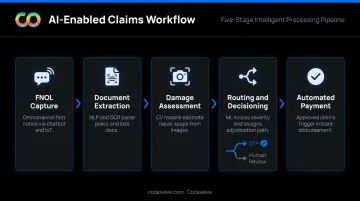

A modern IA-enabled claims workflow looks like this:

- FNOL capture — AI chatbots or IoT device data collect first notice of loss details automatically, without requiring a phone call

- Document extraction — NLP and OCR pull relevant data from submitted forms, medical records, and repair estimates

- Damage assessment — computer vision models analyze photos to estimate repair costs or identify inconsistencies

- Routing and decisioning — ML models flag complex or potentially fraudulent claims for human review; straightforward cases move to straight-through processing (STP)

- Payment — approved claims trigger automated payment without manual intervention

STP is the end goal for eligible claim types. Lemonade's AI-powered claims system demonstrates what a fully automated FNOL-to-settlement workflow looks like at scale: according to Lemonade's SEC filing, eligible claims can be paid in as little as three seconds — no paperwork, no human involved for standard cases.

For more complex portfolios, Aviva's results show what AI can do even for harder claims. McKinsey's documentation of Aviva's AI program found it cut average liability-assessment time for complex cases by 23 days, improved claim-routing accuracy by 30%, and reduced customer complaints by 65%.

Automated Underwriting

Manual underwriting was built for a world where pulling data meant phone calls and paper files. Automated underwriting rewires the entire process.

A modern workflow connects to credit data, medical records, property databases, and applicant forms simultaneously. ML models score risk profiles against historical data, approve standard applications without human review, and flag edge cases with a risk summary already prepared for the underwriter.

The speed difference is significant. Munich Re reports that automated life underwriting systems can deliver coverage decisions in minutes rather than hours or days — a fundamental shift in what applicants experience.

Beyond speed, the shift is from reactive to predictive. ML models continuously learn from historical claims data, refining risk scores over time and enabling more accurate, competitively priced premiums.

Fraud Detection and Prevention

Insurance fraud costs US consumers at least $308.6 billion annually, according to the Coalition Against Insurance Fraud — roughly $932 per person and $3,750 per family. It also occurs in approximately 10% of all property-casualty losses.

ML-based fraud detection trains on historical fraudulent claim patterns, including:

- Duplicate submissions across policies or claimants

- Unusual claim timing relative to policy age

- Inflated repair costs inconsistent with damage photos

- Behavioral anomalies in how claimants fill out forms

The models run in real time, flagging suspicious claims before payment rather than discovering fraud during post-payment audits.

Behavioral analytics adds another layer. Systems monitor policyholder interactions — claim frequency, form-filling patterns, query behavior — to surface anomalies that suggest staged accidents or organized fraud rings before any payout occurs.

Aviva's investment in advanced analytics and ML detected 14% more fraudulent claims year-over-year in 2024, identifying more than 12,700 suspect claims worth £127M (~$161M).

Policy Administration and Compliance

These two areas are often treated separately but share the same automation logic: high-volume, rules-driven processes that consume staff time and introduce risk when done manually.

Policy administration — issuing policies, processing endorsements, managing renewals, updating billing — can be largely automated with RPA bots that pull data across legacy systems, auto-generate documents, and trigger policyholder communications at key milestones.

Regulatory compliance carries the highest stakes. IA applies current regulatory rules consistently at every transaction, generates defensible audit trails automatically, and flags policy exceptions or reporting gaps in real time. For insurers operating across multiple states with different rule sets, this consistency is a compliance requirement, not just an efficiency gain.

Business Benefits of Intelligent Automation for Insurers

Intelligent automation delivers measurable gains across every major function in an insurance operation:

| Benefit | What It Looks Like in Practice |

|---|---|

| Cost reduction | Eliminating labor cost on high-volume repetitive tasks; same headcount handles greater volume |

| Faster turnaround | Claims and policy decisions compressed from days to hours or minutes for eligible cases |

| Accuracy improvement | Consistent data validation at every step; McKinsey reports 3%-5% better claims accuracy from AI-enabled workflows |

| Scalability | Premium volume grows without proportional headcount increases |

| Workforce reallocation | Underwriters handle complex risk; adjusters manage disputed cases; staff focus on advisory interactions |

The customer experience dimension deserves particular attention. J.D. Power found that 52% of customers rating their digital claims experience poor or just OK were likely to leave or not renew — versus just 4% of those who rated it excellent. The quality of automated touchpoints directly affects retention.

The same research found satisfaction dropped 60-70 points when property claim customers who preferred telephone contact were forced into digital-only channels. That gap makes the design choice clear: automation that ignores channel preference doesn't just frustrate customers — it accelerates churn.

Key Challenges to Address Before Adopting Intelligent Automation

Data Readiness and Legacy Integration

IA depends on clean, connected data. Most insurers run on fragmented legacy systems with siloed policy, claims, and billing data — meaning bots cannot reliably access what they need without a foundational integration layer.

A data fabric or API middleware layer creates a unified data layer that allows automation to pull from multiple source systems without requiring each to be rebuilt. Skipping this step produces brittle automation that breaks down whenever data is missing or inconsistent — requiring constant human intervention to compensate.

Codewave addresses this in early project phases by mapping existing data flows, API availability, and system constraints before any automation is deployed. Their modular architecture connects disparate data sources in real time without requiring full core system replacements.

Regulatory Variability and Explainability

US insurance is regulated at the state level. An automated underwriting or claims decisioning system must be configurable to different rule sets across jurisdictions — and in some states, insurers must be able to explain how an automated decision was reached.

This means compliance and legal stakeholders need to be involved from the start of any IA initiative, not brought in after the technology is built. Rule engines must be maintained as regulations evolve, and audit trail generation needs to be built into the architecture rather than retrofitted.

Building Employee and Customer Trust

Technical and regulatory readiness matter, but adoption ultimately depends on trust — from both staff and customers. Not every policyholder wants a fully automated claims experience. Forcing digital-only channels on customers who prefer human interaction actively harms satisfaction scores, as J.D. Power data shows.

A hybrid model is more effective: automation handles routine, low-complexity cases; human handlers take sensitive, complex, or disputed situations. Communicate this clearly to both staff and customers — framing IA as expanding capacity and quality, not replacing judgment.

How to Get Started with Intelligent Automation in Insurance

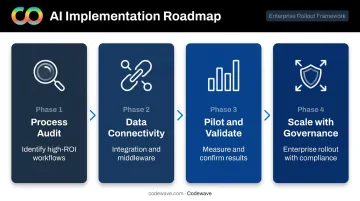

A phased approach consistently outperforms attempting to automate everything simultaneously:

Phase 1 — Process audit Identify high-volume, high-error, time-intensive workflows that offer clear ROI. Claims data entry, policy renewals, FNOL intake, and compliance reporting are typical early candidates. Avoid complex, judgment-heavy workflows in the first phase.

Phase 2 — Data connectivity Before deploying automation tools, confirm that the systems your bots will interact with can reliably share data. This may involve API integrations, middleware, or a data fabric layer. Without this, automation will fail unpredictably.

Phase 3 — Pilot and validate Deploy in a controlled environment, measure against defined KPIs (processing time, error rate, throughput), and validate results before scaling. Codewave's QuantumAgile™ methodology supports this stage specifically — it's built to validate outcomes in days rather than months, letting insurers confirm ROI before committing to enterprise-wide rollout.

Phase 4 — Scale with governance Expand to additional workflows with compliance rules and audit trails built in. Maintain human oversight on edge cases and ensure the hybrid model is operationally clear.

Codewave's ImpactIndex™ outcome-based model aligns directly with this phased approach: clients pay for measurable results like reduced processing time, improved data accuracy, and lower fraud rates — not just technology delivery. For insurance organizations ready to move from strategy to deployed outcomes, that distinction is what separates vendors from partners.

Frequently Asked Questions

What is intelligent automation for insurance claims processing?

Intelligent automation for claims combines AI, RPA, NLP, and computer vision to automate the entire claims process — from FNOL data capture and document extraction to fraud assessment and payment. The result is faster settlement times and reduced manual effort, with human handlers reserved for complex or disputed cases.

What is an example of intelligent automation in insurance?

Lemonade's AI-powered claims process is one of the clearest examples: their system automatically analyzes claim data, cross-references policy terms, checks for fraud indicators, and approves straightforward claims in as little as three seconds, all without human involvement for standard cases.

How does intelligent automation differ from traditional RPA in insurance?

Traditional RPA executes fixed, rule-based tasks — copying data between systems, filling forms. Intelligent automation layers in AI and ML to handle unstructured data, make contextual decisions, and improve over time — enabling complex workflows like risk scoring, document classification, and fraud pattern detection that standard RPA cannot touch.

What are the biggest challenges of implementing intelligent automation in insurance?

Three hurdles consistently slow implementation:

- Legacy system fragmentation — integration work is required before automation can function reliably

- Regulatory variability across states — configurable rule sets and audit capabilities must be built in

- Employee and customer trust — a transparent human-automation hybrid model outperforms a hard cutover

Can intelligent automation handle regulatory compliance in insurance?

Yes — IA can automate compliance tasks such as validating policies against current regulations, generating audit trails, and flagging reporting gaps. However, the underlying rules must be configured and maintained by compliance teams as regulations change. Human oversight of those rule sets remains essential.

How long does it take to see ROI from intelligent automation in insurance?

Insurers that start with high-volume, well-defined processes like claims data entry or policy renewal triggers can see measurable efficiency gains within weeks of deployment. Broader enterprise transformation typically takes 6–18 months, depending on legacy integration complexity and change management scope.