Introduction

Banking has always moved deliberately — built on regulation, risk management, and institutional caution. Yet according to EY-Parthenon's 2025 survey, 77% of banks have already launched or soft-launched generative AI applications, up from 61% just two years ago. That pace of adoption — inside one of the most regulated industries on earth — signals a genuine inflection point.

The pressure driving adoption is real. Banks are contending with:

- Compressing margins that demand operational efficiency

- Customers who expect instant, personalized service across every channel

- Compliance burdens that expand with each regulatory cycle

- Fraud tactics sophisticated enough to outrun legacy detection systems

Traditional tools — rules-based systems, manual workflows, siloed data — struggle to keep pace with any of these pressures simultaneously.

This article covers where GenAI stands in banking today, which use cases are generating the most measurable impact, what institutions are actually gaining, the risks worth taking seriously, and how to move from pilot to production without the failures that derail most programs.

Key Takeaways

- 77% of banks have launched or soft-launched GenAI applications, with 89% expecting major transformative benefits within two years

- Front-office applications (customer service, fraud, personalization) account for 43% of production deployments — the highest share of any category

- Only 16% of GenAI use cases reach full deployment; governance and data quality are the primary barriers

- McKinsey projects $200–$340 billion in additional annual value to banking from GenAI

- Mid-market institutions can achieve comparable outcomes to large banks with the right implementation approach

The State of Generative AI in Banking Today

The industry has moved well past proof-of-concept. Banks are now scaling production deployments and measuring business outcomes.

From Experimentation to Enterprise Scale

McKinsey estimates GenAI could add $200–$340 billion in annual value to the banking sector, equivalent to 9–15% of operating profits. That's not a distant projection: 89% of banks expect major transformative benefits within two years, per EY-Parthenon.

What makes this shift meaningful is what GenAI can actually do that older tools cannot:

- Generates new content rather than executing predefined rules

- Synthesizes unstructured data across documents, voice, and text formats

- Enables human-like interaction that traditional ML and RPA can't replicate

Despite the momentum, most automation work still runs on older technologies. Only 28% of automation use cases currently in development or implemented by banks use GenAI or agentic AI — meaning the majority of automation work still runs on older technologies.

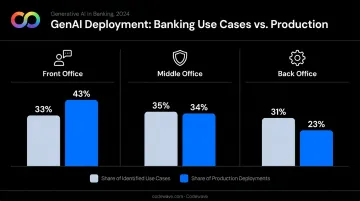

Where GenAI Is Deployed Across the Bank

Production deployments break down as follows, based on EY's March 2025 survey:

| Area | Share of Identified Use Cases | Share of Production Deployments | |------|-------------------------------|----------------------------------|\n| Front Office | 33% | 43% | | Middle Office | 35% | 34% | | Back Office | 31% | 23% |

Front-office applications — customer service, personalization, sales support — have reached production at the highest rate. The ROI is more immediate and measurable, which accelerates executive buy-in and budget allocation.

Key Use Cases: Where GenAI Is Making the Biggest Impact

Customer Experience and Intelligent Support

GenAI-powered virtual assistants now handle account inquiries, transaction disputes, loan guidance, and personalized product recommendations — in real time, across multiple languages, around the clock. Unlike scripted chatbots, LLM-based assistants analyze account history and inferred intent to deliver contextually relevant responses.

Klarna's OpenAI-powered assistant illustrates the scale this enables. Operating across 35 languages in 23 markets, it handled 2.3 million conversations in its first month — roughly two-thirds of all customer service interactions. Average resolution time dropped from 11 minutes to under 2 minutes. The company estimated a $40 million profit improvement for 2024, equivalent to the work of approximately 700 full-time agents.

The implication for banks: exponentially more interactions handled at consistent quality, without proportional cost growth. Volume scales; headcount doesn't have to.

Fraud Detection and Risk Management

Legacy fraud systems operate on fixed rules: if a transaction exceeds a threshold or originates from an unusual location, flag it. GenAI works differently: it identifies anomalous patterns across massive transaction datasets, including fraud types that haven't been explicitly defined yet. Models learn continuously from new data, improving detection rates while reducing false positives that frustrate legitimate customers.

Mastercard's Decision Intelligence Pro demonstrates the potential: their GenAI-enhanced system improves fraud detection rates by 20% on average, with improvements as high as 300% in some instances.

For financial institutions building similar capabilities, Codewave's fintech implementations have targeted outcomes including 99% reduced fraud risk and 90% fewer data errors — reflecting what well-governed AI solutions can deliver when data quality and model architecture are properly addressed.

Loan Processing, Credit Scoring, and Underwriting

Traditional credit scoring relies on structured data: credit history, debt-to-income ratios, employment records. GenAI expands the picture by processing transaction histories, spending patterns, and alternative data signals to build a more complete risk assessment. The benefits run in both directions:

- Lenders get more accurate risk pricing with fewer blind spots

- Borrowers without conventional credit histories gain access to fairer assessments

- Underwriters spend less time on manual document review

McKinsey documented a commercial bank using GenAI to cut climate-risk questionnaire processing time by 90%, one example of how document-heavy workflows compress once AI handles extraction and categorization.

On the customer-facing side, GenAI chatbots guide borrowers through mortgage and loan applications step by step, reducing errors and completion time. Kasisto's KAI-GPT, piloted by Westpac as the first banking-specific LLM, was built for exactly this context: mortgage officers and customer agents navigating complex, document-heavy processes where domain precision matters.

Interpretability isn't optional here. The CFPB has made clear that lenders using AI in credit decisions must provide specific, accurate adverse-action explanations, making explainability a compliance requirement rather than a technical preference.

Back-Office Automation and Compliance Reporting

Regulatory reporting, document extraction, policy summarization, and compliance review have historically consumed enormous amounts of analyst time. GenAI compresses that dramatically.

SouthState Bank deployed enterprise ChatGPT for bankers, using it to compose correspondence, summarize regulatory documents, and analyze policy. Tasks that previously took 15 minutes completed in seconds. The productivity gains were immediate enough that the bank described the technology as "worth all the hype," per American Banker.

On invoice and financial data processing, McKinsey documented an LLM-based categorization system that helped one European institution reduce costs by 10% of its spend base — a meaningful figure for back-office operations at scale.

The Real Business Impact: What Banks Are Actually Gaining

Across multiple credible sources, the data is consistent — and the gains are significant.

Revenue and Efficiency Gains

- 58% of banks report a positive revenue uplift of 6–20% from current GenAI applications, with 79% expecting continued uplift over the next two years (EY-Parthenon)

- PwC's analysis projects up to a 15 percentage-point improvement in bank efficiency ratios for institutions that fully embrace AI

- One institution cited by PwC achieved a 40% decrease in costs to verify commercial banking clients through AI-driven onboarding tools

These results reflect institutions that invested in the right prerequisites: solid data infrastructure, governance frameworks, and change management alongside the technology itself. Without those foundations, the numbers don't follow.

Where the Value Concentrates

56% of GenAI banking use cases target internal efficiency — cost reduction leads. The revenue case is building alongside it:

- Hyper-personalization surfaces the right product to the right customer at the right moment, turning behavioral data into cross-sell and upsell revenue

- Faster dispute resolution and proactive financial guidance improve retention rates

- AI-assisted relationship managers handle larger books of business without service quality declining

McKinsey estimates GenAI can improve productivity in core corporate and investment banking activities by 30–90%, with analysts cutting pitch book creation time by around 30% — hours that add up fast across thousands of analysts.

What This Means for Mid-Market Institutions

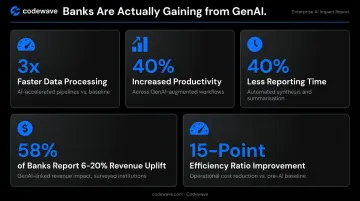

These gains aren't locked behind JPMorgan-scale engineering budgets. Mid-market institutions are reaching comparable outcomes when the implementation is disciplined. Codewave's work across fintech and financial services clients has produced benchmarks including 3x faster data processing, 40% increased productivity, and 40% less reporting time. The prerequisite is the same at any institution size: solid data foundations and a structured approach to rollout.

Challenges and Risks That Banks Must Navigate

The gap between ambition and execution is significant. Only 16% of GenAI use cases reach full deployment, and 40% of implemented use cases fail to meet expectations or are discontinued — per EY's March 2025 survey data. Knowing where deployments break down is the starting point for getting them right.

Data Privacy and Security

GenAI requires access to sensitive financial data at scale. That creates exposure: data breaches, unauthorized model access, and third-party vendor vulnerabilities all expand the attack surface. GDPR and CCPA compliance adds further complexity, particularly when data is processed by external model providers.

BNP Paribas addressed this by partnering with Mistral AI — gaining access to frontier model capabilities while maintaining greater control over where data flows and how models are deployed across business lines. Data governance, it turns out, isn't just a security concern — it's the foundation for everything that follows.

Governance and Implementation Failures

The primary barriers to successful deployment, per EY, are:

- Regulatory compliance complexity

- Data quality limitations

- Insufficient alignment between IT, compliance, risk, and business units

Banks that would restart their GenAI journey identify improved governance as the single most important change they would make. The technology rarely fails on its own. What fails is the operating model built around it.

Model Reliability and Bias

GenAI models hallucinate — they produce confident, plausible-sounding outputs that are factually incorrect. In a customer service context, that's a reputation risk. In a credit decision context, it can trigger regulatory action and legal exposure simultaneously.

Models trained on biased historical data can also produce unfair lending outcomes, which creates both legal exposure and reputational harm. The FSB has specifically flagged model risk, explainability gaps, and data quality as financial stability concerns at the system level.

Banks need:

- Explainability frameworks that satisfy regulatory audit requirements

- Human-in-the-loop review at high-stakes decision points (credit decisions, fraud flags, compliance determinations)

- Rigorous ongoing evaluation protocols, not just pre-deployment testing

From Pilot to Production: How Banks Should Approach GenAI Adoption

Most GenAI programs fail not because the technology doesn't work — they fail because institutions skip the prerequisites.

Start With Use Case Prioritization

The most common mistake is selecting technology before defining the problem. Banks should identify where GenAI delivers the highest value relative to its risk profile:

- High value, lower risk: Customer-facing personalization, internal knowledge search, document summarization

- High value, higher governance requirement: Fraud detection, credit underwriting, regulatory reporting

- Emerging, careful staging needed: Agentic AI for autonomous decision workflows

The rule of thumb: GenAI fits generative and personalization-heavy applications; traditional ML and RPA handle structured, repetitive processes best.

Fix the Data Foundation First

GenAI is only as good as the data feeding it. Banks that identify data-related challenges as their top implementation barrier — poor governance, inconsistent quality, siloed systems — will struggle to convert pilots into production at any scale. Solving data readiness early also makes the governance work that follows significantly easier.

Build Governance Into the Program Architecture

79% of banks said they would prioritize improving governance if restarting their GenAI journey. That means engaging compliance, risk, legal, and business unit leaders from the start — not bringing them in after the technical build is complete.

Practical governance requirements include:

- Formal AI governance committees with clear accountability

- Defined escalation paths for model failures or unexpected outputs

- Regulatory alignment with NIST AI RMF and applicable banking frameworks

- Documented human-override protocols at key decision points

Choose Implementation Partners Carefully

For institutions without deep in-house AI engineering, a specialized implementation partner reduces the execution risk that causes most pilot failures. Codewave works with fintech and financial services clients through its ImpactIndex™ model — an outcome-based engagement structure where clients pay for measurable results, not just deployment activity. Its core stack (TensorFlow, Apache Kafka, Snowflake) handles the data volume and real-time processing demands that financial services AI routinely requires.

Frequently Asked Questions

How can generative AI be used in banking?

GenAI's primary banking applications include customer service chatbots, fraud detection, loan underwriting, compliance reporting, personalized marketing, and back-office document processing. Its key strength is processing unstructured data (emails, documents, transaction narratives) and generating human-like responses at scale that rule-based systems can't replicate.

Which AI is best for banking?

The right AI depends on the use case. GenAI excels at personalization and content generation; traditional ML and RPA handle structured, repetitive workflows more efficiently; and agentic AI is emerging for autonomous, decision-intensive processes. Banks that perform best use a hybrid approach — matching the right technology to each use case based on complexity, risk, and ROI profile.

How is JPMorgan Chase using AI?

JPMorgan Chase deployed LLM Suite, its proprietary generative AI assistant, to more than 60,000 employees by August 2024 for drafting, summarization, and research tasks. Reuters reported the tools helped staff boost sales and add clients during market volatility — and American Banker named it a 2025 Innovation of the Year.

What are the biggest risks of generative AI in banking?

The top risks include data privacy exposure, model hallucinations, bias in credit decisions, regulatory complexity, and high implementation failure rates. Forty percent of use cases fail to meet expectations — and most failures trace back to data quality and governance gaps, not the technology itself.

How does generative AI improve fraud detection in banking?

GenAI analyzes vast transaction datasets to identify anomalous patterns — including fraud types not yet explicitly categorized — adapts to emerging threats in real time, and processes data at speeds that legacy rule-based systems can't match. Mastercard's Decision Intelligence Pro improved fraud detection rates by 20% on average, with improvements as high as 300% in some instances.

Is generative AI replacing bank employees?

No — it's augmenting them. Routine, manual tasks are being automated, but complex decisions, regulatory accountability, and relationship management still require human judgment. Most roles are shifting toward AI oversight, exception handling, and strategic analysis rather than being eliminated. The productivity gains come from doing more with the same team, not from headcount reductions alone.