Introduction

Banks have spent the last decade digitizing — moving paper to pixels, branches to apps, manual approvals to rules-based workflows. Yet despite this investment, most institutions still rely on human handoffs to reconcile accounts, process loan applications, and compile compliance reports. That gap between "digital" and "intelligent" now shows up directly in operating costs and lost speed-to-market.

Agentic AI closes that gap. Unlike predictive models or chatbots that surface information for humans to act on, agentic systems plan, execute, and iterate across multi-step workflows with minimal human prompting. A single loan moves from scoring through origination, documentation, compliance checks, and post-close monitoring — all within one connected system.

According to BCG, AI agents have the potential to increase bank profitability by 30% and reduce costs by 30–40% by 2030. That represents a structural shift in how banks operate, not a marginal efficiency win.

This article covers where agentic AI creates the most impact across front, middle, and back office operations, why the competitive window is narrowing, and how banks can build a practical path to implementation.

Key Takeaways

- Agentic AI executes complete financial workflows autonomously — from loan origination to compliance reporting — replacing human decision loops, not just supporting them

- Banking functions most disrupted: customer onboarding, fraud detection, credit decisioning, compliance monitoring, and deposit management

- Unlike rules-based automation, agentic systems adapt to new data and improve continuously over time

- API integration quality — not geographic scale — is becoming the defining competitive advantage in banking

- Governance, explainability, and human oversight must be built into the architecture from day one

What Is Agentic Banking? From Reactive Tools to Autonomous Execution

Defining the Shift

Traditional banking AI — predictive models, chatbots, rules engines — produces outputs that humans interpret and act on. A fraud score flags a transaction; a compliance officer reviews it. A credit model returns a probability; an underwriter makes the call.

Agentic AI operates differently. McKinsey describes agentic systems as proactive, goal-driven collaborators that combine autonomy, planning, memory, and integration — taking inputs, reasoning across multiple data sources, executing actions across connected systems, and refining behavior based on outcomes, without requiring a human prompt at each step.

In banking terms: the system doesn't just identify the refinancing opportunity. It evaluates terms, calculates net benefit, prepares documentation, and initiates the workflow.

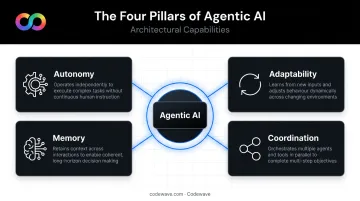

The Four Architectural Capabilities That Matter

Four capabilities separate agentic systems from earlier automation approaches:

- Autonomy — acts on defined objectives without step-by-step human direction

- Adaptability — updates behavior as new data arrives, market conditions shift, or regulatory requirements change

- Memory — retains context from prior interactions to inform future decisions

- Coordination — operates simultaneously across multiple tools, APIs, and other agents

What Agentic Banking Is Not

Agentic AI is not full automation without oversight. The human role shifts from initiating each transaction to setting strategic boundaries and reviewing exceptions.

Banks define the operational boundaries agents work within:

- Guardrails: autonomy thresholds, escalation triggers, and audit trail requirements set by the institution

- Human review preserved: large credit approvals and regulatory filings still require human sign-off, by both design and regulatory requirement

How Agentic AI Transforms Banking Operations: Front, Middle, and Back Office

The most effective frame for understanding agentic AI's impact is the three-layer banking model (front, middle, and back office). Unlike siloed automation that optimizes one process at a time, agentic systems connect all three layers into a single intelligent workflow.

Front Office: Goal-Driven Customer Experience

Today's self-service banking is menu-driven. A customer wants to reduce debt : they navigate to a calculator, transfer funds manually, maybe call a specialist. Agentic AI replaces that friction with goal-driven assistance — the customer states an objective, and the agent translates it into action.

This means reallocating funds, adjusting spending limits, flagging refinancing opportunities, or initiating product workflows, all within a single interaction and without handoffs or form navigation.

Consumer readiness is already there. Salesforce's Connected Financial Services Report found 77% of consumers are interested in AI that actively prevents and detects fraud. J.D. Power found 51% of consumers already use AI tools for financial advice or information. The demand for capable AI in banking isn't theoretical — it's being expressed in behavior.

Capgemini's World Retail Banking Report found only 4% of banks open accounts within one day, and 18% of customers abandon applications mid-process. Agentic systems that complete onboarding within a single session (verifying identity, running compliance checks, activating accounts) directly address this attrition.

Middle Office: Credit, Fraud, and Compliance

Credit decisioning is where agentic AI compresses days into minutes. A single agentic loan origination system handles the full cycle:

- Ingests application data and cross-references external sources

- Performs risk assessment across cash flow and sector exposure

- Generates a credit structure proposal with supporting documentation

- Runs compliance checks and maintains a full audit trail

The same agent monitors the borrower post-origination, adjusting credit limits or triggering restructuring if conditions deteriorate.

Upstart's 2024 annual report shows more than 91% of Upstart-powered loans were fully automated, with borrowers approved instantly and no human intervention required.

Fraud detection is the area with the strongest evidence base for agentic performance. HSBC reports AI finds 2–4x more financial crime than prior systems, with 60% fewer false positives. Mastercard's generative AI enhancements boost fraud detection by 20% on average — and up to 300% in specific instances — operating across 1 trillion data points in under 50 milliseconds.

Compliance monitoring shifts from retrospective to continuous. Instead of periodic manual reviews, agentic systems scan transactions in real time, track regulatory updates, and generate audit-ready reports on demand.

Back Office: The Digital Engine

The back office is where agentic AI delivers the most immediate cost impact. Document extraction, internal reporting, regulatory data pulls, and resource scheduling (all currently reliant on manual effort) can be automated end-to-end.

McKinsey estimates that moderate agentic AI adoption could enable banking cost reductions of 15–20%. BCG puts the upper range at 30–40% by 2030. Accenture estimates early adopters could see 22–30% productivity gains and 600 basis points higher revenue growth over three years.

Codewave's back-office automation work across financial services clients demonstrates what this looks like in practice: 3x faster data processing, 90% reduction in human errors, 25% lower operational costs, and approximately three weeks saved per month in manual data work — achieved through AI-OCR, automated compliance workflows, and real-time transaction monitoring pipelines.

Without this back-office foundation, even the most sophisticated front-office AI runs into operational ceilings. The infrastructure determines what the experience can actually deliver.

The Competitive Pressure: Why Banks Cannot Afford to Wait

Deposits Are No Longer Sticky by Default

Deposits stay put today largely because switching is inconvenient. That friction is the foundation of stable, low-cost funding that supports loan growth. Agentic AI eliminates it: a customer's agent can be configured to automatically move cash balances between institutions for a marginal rate advantage — continuously, without manual effort.

McKinsey identifies deposits as the top profitability lever for retail bank CEOs and notes that sophisticated deposit management directly boosts margins and customer loyalty. When AI agents make optimization effortless, that management capability shifts to the customer side. Banks can no longer assume deposit inertia will hold — the advantage has to be earned continuously.

API Compatibility Is the New Competitive Moat

Geographic presence and brand familiarity are losing ground to a different kind of competitive advantage: API compatibility and integration quality.

Banks with agent-friendly interfaces, robust data feeds, and automation-ready workflows will capture flow from institutions that still require manual processes. This dynamic levels the playing field in a real way:

- A community bank with superior digital integration can outcompete a larger institution running rigid legacy infrastructure

- API quality — not branch count — determines which institutions agents are configured to route funds through

- Institutions that lag on integration lose business passively, without a single customer complaint

UK open banking reached 16.5 million user connections in 2025, with 24 billion successful API calls — up 27% year over year. Finastra found 47% of financial institutions are modernizing via API-led technology and cloud migration. The infrastructure shift is already underway. Banks still relying on manual-heavy processes are watching that window close.

Risks, Governance, and the Human-AI Balance

Deploying agentic AI in banking without governance infrastructure is not a calculated risk: it's a compliance failure waiting to happen. Three risk categories require architectural responses, not policy statements.

Algorithmic Bias

Agentic systems making loan approvals, fraud investigations, or credit limit decisions at scale can reinforce harmful patterns when trained on incomplete or skewed data. Academic research (Fuster et al., Bartlett et al.) documents disproportionate impacts on Black and Hispanic borrowers in ML-driven mortgage credit markets. The CFPB is explicit: black-box AI does not exempt lenders from explaining credit denials.

Required responses:

- Explainable AI (XAI) models that produce traceable decision logic

- Diverse, representative training datasets

- Regular fairness audits across demographic segments

Data Privacy and Security

Agentic systems operate across multiple environments, APIs, and external agents, dramatically expanding the attack surface. CISA warns that two-way tool/API integration exposes agents to arbitrary instructions through compromised external sources. Required controls include approved tool allow lists, sandboxing, logging, and regular red teaming.

NIST identifies agent identity and authorization as a distinct security gap. Authenticating AI agents before they execute consequential actions is a separate architectural requirement from traditional user access management — one that most existing controls don't address.

Regulatory Accountability

The EU AI Act classifies creditworthiness AI as high risk. The Fed/OCC's revised model risk guidance (SR 26-2, 2026) requires effective challenge, conceptual soundness review, and ongoing monitoring for banking AI — particularly at institutions over $30 billion in assets. The FCA identifies the Senior Managers and Certification Regime as the accountability mechanism for AI use in UK financial services.

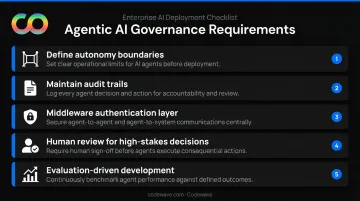

When an agentic system autonomously approves a loan or adjusts a credit limit, the bank remains responsible. That accountability requires concrete infrastructure, not just policy language:

- Define autonomy boundaries for each agent type before deployment

- Maintain audit trails at every decision point

- Middleware layers that enforce authentication and access policies across AI workloads

- Require human review for high-stakes decisions before final execution

- Adopt evaluation-driven development (EDD) to continuously measure agent performance against defined quality thresholds

Governance infrastructure also shapes how the workforce adapts. Agentic AI works best when it elevates human roles rather than displacing them, moving employees from routine execution into exception handling, relationship management, and AI oversight. That shift requires investment in data literacy and clear communication about how autonomous systems make decisions.

A Practical Roadmap for Implementing Agentic AI in Banking

BCG found fewer than one in four banks are currently ready for AI disruption, and only 5% are positioned for long-term advantage through superior AI maturity. That gap between ambition and readiness is wide. Getting the sequence right determines whether agentic AI scales or stalls.

Step 1: Start With High-Value, Lower-Risk Pilots

Begin with workflows where agentic AI can demonstrate fast, measurable ROI without high regulatory complexity:

- Credit onboarding document summaries

- Fraud anomaly escalation and routing

- Internal regulatory reporting automation

- KYC verification and compliance pre-screening

Proving early ROI builds internal momentum and the stakeholder trust required for broader adoption. McKinsey notes that credit-risk memo creation alone could raise productivity by 20–60% — a strong pilot anchor.

Step 2: Build the Foundational Infrastructure First

Scaling agentic AI without the right foundation produces technical debt that becomes harder to unwind. Foundational requirements:

- Clean, connected data architecture — unified data layer spanning CRMs, core banking systems, and external feeds

- Middleware layer that centralizes AI governance, authentication, and access control across all AI workloads

- Integration-ready APIs enabling agentic systems to interact with internal systems and external partners

This means compliance requirements need to be embedded at the architecture level, not added after the fact. Banks that treat infrastructure as a Phase 2 problem consistently hit ceilings when they try to expand agentic systems beyond their initial pilots.

Step 3: Establish a Cross-Functional AI Center of Excellence

An AI Center of Excellence (CoE) brings together AI engineers, compliance specialists, domain experts, and risk managers under a shared governance model. The CoE owns:

- Intake prioritization and use case sequencing

- Toolchain standards and evaluation frameworks

- Audit trail design and exception thresholds

- External partner and vendor engagement

For banks and fintechs building this function from scratch, working with an implementation partner that has stood up CoEs across multiple regulated industries can compress the timeline considerably. Codewave has done this across finance, healthcare, and adjacent sectors — establishing governance structures that let teams ship quickly while keeping audit and compliance requirements intact.

Step 4: Define Human Oversight Before Deployment

Governance designed retroactively creates compliance gaps. Before any agent goes live, define:

- Which decisions require mandatory human review

- What exception thresholds trigger escalation

- How audit trails will be maintained and accessed by regulators

The accountability structure has to be in the architecture, not bolted on afterward.

Frequently Asked Questions

What is agentic AI in banking?

Agentic AI refers to AI systems that autonomously plan and execute multi-step financial tasks — such as loan processing, compliance monitoring, or personalized financial planning — with minimal human prompting. It goes beyond traditional AI tools that only surface information for humans to act on.

How is agentic banking different from traditional banking automation?

Traditional automation follows fixed rules and requires humans to act on AI outputs. Agentic AI reasons across data, initiates actions across multiple systems, adapts to new information, and retains memory of past interactions. The result is continuous, self-improving workflows rather than isolated task execution.

What banking operations benefit most from agentic AI?

The highest-impact areas are customer onboarding and credit decisioning (front and middle office), real-time fraud detection and compliance monitoring (middle office), and internal document processing, regulatory reporting, and resource optimization (back office).

What are the biggest risks of deploying agentic AI in financial services?

Three primary risk categories demand attention:

- Algorithmic bias in high-stakes decisions such as loan approvals and fraud flagging

- Data privacy and security vulnerabilities from expanded attack surfaces across APIs and external agents

- Regulatory accountability gaps when autonomous systems make consequential decisions without traceable human oversight

How should a bank begin its agentic AI implementation?

Start with a pilot focused on high-value, lower-risk workflows — credit onboarding summaries or fraud escalation are good entry points. Build clean data infrastructure and a governance framework before scaling, then establish a cross-functional AI CoE to own standards and oversight.

Can community banks and credit unions compete with large banks using agentic AI?

Yes. Agentic AI makes API integration and workflow automation the new competitive differentiator, not physical scale. Smaller institutions with superior digital integration and agent-friendly platforms can capture deposits and loan volume from larger competitors whose legacy infrastructure still depends on manual processes.