This article covers what multi-agent AI is, how its four-layer architecture works, the highest-value use cases in finance (fraud, lending, insurance, compliance), how to choose the right orchestration pattern, and what governance looks like in practice.

Key Takeaways

- Multi-agent AI deploys specialized agent networks where each agent handles a distinct role, collaborating across complex financial workflows

- Top use cases: fraud detection, loan processing, insurance claims, portfolio management, AML/KYC compliance

- Architecture runs across four layers: data ingestion, specialized agents, orchestration, and LLM reasoning, each purpose-built for its function

- Three coordination patterns exist — sequential, hierarchical, and swarm — and matching the right one to your use case determines whether the system scales or fails

- Governance (data permissions, service boundaries, reasoning limits) must be defined before production deployment

What Is Multi-Agent AI and When Does Finance Actually Need It?

Multi-agent AI is a coordinated network of specialized AI agents that each handle a defined task and collaborate through shared protocols to execute complex, multi-step workflows. Rather than one monolithic model, MAS deploys what Cognizant calls "digital specialists"—each agent combines an LLM for reasoning with a code layer for action execution such as calling APIs or retrieving data.

This differs from single-agent models or RAG-based systems that handle isolated queries. A RAG model works well for FAQ chatbots or document summarization. MAS becomes necessary when workflows cross departments, integrate multiple data systems, or require sequential decisions—comparing products across banks, processing a loan from application to approval, or managing an end-to-end insurance claim.

When to choose MAS over single-agent:

- Workflow complexity: Tasks require decentralized coordination across heterogeneous data sources

- Parallel processing: Multiple specialized roles must operate simultaneously (not sequentially waiting on one model)

- Iterative refinement: Decisions require feedback loops between agents

- Regulatory auditability: Each decision step must be traceable to a specific agent

Microsoft recommends evaluating complexity first: "Use the lowest level of complexity that reliably meets your requirements." Coordination overhead, latency, and cost all increase with multi-agent architectures—so adopt MAS only when single-agent approaches fall short.

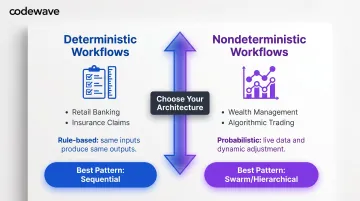

Deterministic vs. Nondeterministic Finance Workflows

Which type of MAS architecture fits a financial use case depends on its underlying logic. Finance breaks cleanly into two categories:

| Workflow Type | Examples | Agent Behavior |

|---|---|---|

| Deterministic | Retail banking, insurance claims | Rule-based; same inputs produce same outputs. A claims agent checks policy terms against incident data and approves or denies based on fixed criteria. Suits sequential patterns with strict audit trails. |

| Nondeterministic | Wealth management, algorithmic trading | Probabilistic; agents process live market feeds, run Monte Carlo simulations, and adjust recommendations dynamically. Static rules don't apply when market variables shift constantly. |

The Core Architecture of Multi-Agent AI Systems in Finance

Multi-agent systems in finance stack four distinct layers, each with a defined responsibility.

Data Layer

The data ingestion and normalization layer continuously collects, cleans, and standardizes structured data (transaction logs, pricing feeds, credit scores) and unstructured data (client communications, regulatory documents, news sentiment) from multiple sources into formats agents can reliably consume.

Data quality here directly determines agent output reliability. If a fraud detection agent receives inconsistent transaction formats or a loan underwriting agent processes incomplete credit reports, downstream decisions degrade. This layer must handle:

- Real-time streaming for fraud and trading use cases

- Batch processing for compliance reporting and periodic reviews

- Schema validation to catch malformed data before it reaches agents

- Data lineage tracking for regulatory audit requirements

Agent Layer

The specialized agent layer deploys agents scoped to a specific function: prediction, risk evaluation, trade execution, compliance validation, document extraction. Each agent operates autonomously within its domain.

Narrow scope per agent is what enables accuracy. Cognizant's research confirms that agents overloaded with too many responsibilities degrade in performance—a fraud detection agent that also validates KYC compliance and processes loan applications will fail at all three tasks.

Example agent specialization in loan underwriting:

- Document extraction agent: Pulls applicant data from PDFs and forms

- Credit analysis agent: Retrieves credit scores and payment history

- Income verification agent: Cross-references tax documents and bank statements

- Policy validation agent: Checks eligibility against lending rules

- Risk modeling agent: Calculates default probability and loan-to-value ratios

- Approval agent: Produces pre-approval decision or escalates to human review

Orchestration Layer

The orchestration layer is the system's coordination core. A supervisor or orchestrator agent receives tasks, decomposes them into subtasks, routes each subtask to the right specialized agent, manages data handoffs between agents, and ensures no agent operates outside its defined scope.

AWS maps four primary orchestration patterns for financial services: Workflow (sequential), Swarm (peer-to-peer), Graph (hierarchical supervisor), and Loop (iterative refinement). The orchestrator enforces the chosen pattern and prevents cross-agent interference.

Where monolithic AI models struggle to balance competing objectives — speed vs. accuracy, compliance vs. flexibility — the orchestrator delegates each objective to a specialist agent and synthesizes results. This division of responsibility is what reduces decision errors at scale.

LLM and Reasoning Layer

LLMs power each agent's reasoning—they interpret user intent, decide which tool or service to invoke, and determine what to pass to the next agent in the chain. In high-stakes financial domains, agents connect to domain-specific quantitative tools:

- Factor risk models for portfolio managers

- Monte Carlo simulators for derivatives pricing

- Credit scoring engines for underwriters

- Sanctions screening APIs for compliance agents

Purpose-built financial multi-agent systems earn their complexity here. A specialized portfolio optimization agent integrated with real market data and client risk profiles delivers something a general-purpose chatbot simply cannot: portfolio-level impact modeling tied to a specific client's exposure.

Infrastructure Layer

Infrastructure options include:

- On-premise: Maximum data control, required for highly sensitive financial data

- Cloud (AWS, Azure, Google Cloud): Scalability and elastic compute for peak transaction volumes

- Hybrid: Sensitive data stays local while compute-intensive tasks offload to the cloud

Infrastructure choice must satisfy regional data compliance requirements. Under GDPR, EU customer data must stay within EU data centers. The EBA confirms that AI systems for creditworthiness evaluation are classified as high-risk under the EU AI Act, triggering mandatory safeguards and co-supervision by financial regulators.

Infrastructure must also handle peak transaction volumes without latency degradation. A fraud detection system that slows to a crawl during high-volume periods defeats its own purpose — real-time detection only works if the system responds in real time.

High-Impact Use Cases of Multi-Agent AI in Finance

Fraud Detection

A multi-agent fraud system deploys:

- Data monitoring agent: Real-time transaction surveillance across payment channels

- Anomaly detection agent: Flags behavioral outliers against historical patterns using unsupervised learning

- Decision-making agent: Evaluates flagged transactions, calculates risk scores, and routes high-risk cases to human reviewers

Continuous inter-agent learning makes the system adaptive to new fraud patterns. American Express improved fraud detection by 6% using advanced LSTM AI models, while PayPal improved real-time detection by 10% through 24/7 AI systems—both examples of AI's advantage over rigid rules-based systems that produce high volumes of false positives.

Multi-agent architectures add another layer: instead of one model trying to balance precision and recall, specialized agents optimize for different objectives and the orchestrator synthesizes results.

Loan and Credit Processing

AWS documents a hierarchical graph pattern for "Intelligent Loan Application Processing" where a coordinator agent orchestrates subordinate agents for financial analysis, risk analysis, income verification, and fraud detection.

How the workflow divides:

- Document agent extracts data from applications, tax forms, and bank statements

- Policy agent validates eligibility against lending rules and regulatory requirements

- Fraud detection agent cross-references applicant data against known fraud patterns

- Risk modeling agent calculates default probability and loan-to-value ratios

- Recommendation agent builds a risk-adjusted business case

- Approval agent produces automated pre-approval decisions or escalates to underwriters

This parallel processing compresses turnaround time sharply. Traditional underwriting processes applications sequentially over days; multi-agent systems process in parallel and return decisions in minutes to hours.

Regulatory note: The EU AI Act classifies AI for creditworthiness evaluation as high-risk, triggering mandatory safeguards and distinct compliance obligations depending on whether you're a provider (developed in-house) or deployer (using a third-party system).

Insurance Claims Adjudication

Insurance follows a sequential workflow using deterministic rule-based logic, making it one of the most well-suited MAS use cases in finance:

- FNOL agent (First Notice of Loss) captures incident details and policyholder data via phone or digital channels

- Damage appraisal agent validates claim details against policy rules, cross-references images and medical records

- Fraud detection layer flags anomalies with confidence scores

- Settlement agent triggers payouts for straightforward claims or escalates to human adjusters when confidence falls below thresholds

Cognizant's Auto Claims Process Accelerator achieves 25-30% cycle time reduction, 30% cost-per-claim reduction, and sub-500ms latency from transcription to structured data extraction. The system integrates with Guidewire and Duck Creek platforms and maintains human-in-the-loop oversight—adjusters intervene only when model confidence falls below defined thresholds.

Portfolio Management and Wealth Advisory

Multi-agent systems for wealth management deploy:

- Market analysis agent: Monitors economic indicators, interest rates, sector performance

- Stock performance agent: Tracks individual equities, earnings reports, analyst ratings

- Portfolio optimization agent: Rebalances asset allocations based on risk tolerance and market conditions

- Compliance agent: Ensures recommendations comply with suitability rules and fiduciary standards

- Synthesis agent: Produces client-specific, compliant recommendations

Off-the-shelf tools can't model portfolio-level impact for a specific client. A generic robo-advisor might recommend "buy more bonds." A specialized MAS evaluates the client's current holdings, tax situation, risk profile, and liquidity needs before surfacing any recommendation.

McKinsey documents that AI is rapidly automating technical advisory tasks (tax modeling, scenario planning, portfolio commentary), making technical planning a baseline capability. However, nearly 80% of affluent households still prefer a human relationship over AI-only interfaces—meaning the future is human advisors augmented by multi-agent systems, not replaced by them.

Regulatory Compliance and AML/KYC

Compliance-specific agents run parallel to operational agents, continuously scanning transactions for AML patterns, validating identity against sanctions lists, and generating audit-ready logs.

Nasdaq Verafin's Agentic AI Workforce includes:

- Digital Sanctions Analyst: Reduces bank alert review workload by more than 80%, dispositioning false positives autonomously while escalating true matches

- Digital EDD Analyst: Automates periodic Enhanced Due Diligence reviews, closing low-risk cases without human intervention

The system serves more than 2,600 financial institutions representing over $10 trillion in collective assets. MAS is better suited to compliance than monolithic AI for one structural reason: governance-ready design. Every decision step is traceable to a specific agent, so regulatory audits don't require reverse-engineering a black box.

Codewave's fintech implementations have delivered measurable outcomes including 99% reduced fraud risks and 50% faster invoice processing—results that follow directly from building governance and specialization into the architecture rather than treating them as afterthoughts.

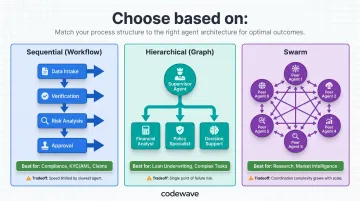

Multi-Agent Architecture Patterns: Choosing the Right Fit

AWS identifies four primary patterns with explicit financial services mappings. Choosing the wrong pattern carries real operational risk: sequential workflows bottleneck under time pressure, hierarchical designs can fail at a single node, and swarm configurations grow unwieldy without tight coordination protocols.

Sequential (Workflow) Pattern

Agents execute tasks one after another in a strict chain, with each agent's output becoming the next agent's input.

Best for: Compliance-driven, auditable processes like KYC/AML verification, claims adjudication, and loan underwriting where accuracy matters more than speed and every step must be logged.

Tradeoff: Speed is limited by the slowest agent in the chain. If the credit analysis agent takes 2 minutes and the income verification agent takes 30 seconds, the entire workflow cannot complete faster than 2.5 minutes.

Example: Insurance claims—FNOL → damage appraisal → fraud check → settlement

Hierarchical (Graph) Pattern

A coordinator or supervisor agent sits at the top of a decision tree, delegating subtasks to specialized subordinate agents. A loan underwriting supervisor orchestrates credit assessment, fraud detection, income verification, and risk modeling agents.

Best for: Workflows that mirror real institutional org structures, providing clear chains of accountability. Systematic decomposition of complex tasks into manageable subtasks.

Tradeoff: Single point of failure risk—if the orchestrator agent fails, downstream processes stall. Redundant failover mechanisms are non-negotiable.

Example: Loan processing—supervisor delegates to document extraction, policy validation, fraud detection, and risk modeling agents, then synthesizes results into approval decision.

Swarm Pattern and Anti-Patterns

In a swarm, agents operate as a collaborative mesh without a strict hierarchy—useful for financial research and analysis where multiple agents (stock analysis, sentiment analysis, financial metrics, company profiling) work in parallel and share findings through shared memory.

Best for: Research generation, market intelligence, scenario analysis where multiple perspectives improve output quality.

Tradeoff: Coordination complexity increases as agent count grows. Without clear protocols, agents may duplicate work or produce conflicting outputs.

These coordination failures point to two anti-patterns that appear most often in swarm and over-engineered architectures — and are worth avoiding from the start:

Large Singleton: Overloading one agent with too many tools, causing confused tool selection and slower performance. An agent with access to 50 APIs will struggle to pick the right one.

Agent Washing: Rebranding simple automation as agentic AI without real multi-agent capability. If your "multi-agent system" is just a chatbot calling a few APIs, it's not a true MAS.

Governance, Security, and Compliance for Multi-Agent Finance AI

Data Governance

Define permission boundaries at the field level—each agent should access only the data required for its specific task. A claims eligibility agent sees relevant policy fields but not unrelated financial records.

Three data types requiring distinct governance:

- Public data (market prices, regulatory filings): Open read access across agent roles

- Internal data (underwriting rules, risk models): Role-based access tied to agent function

- Customer PII/transactional data: Strict controls with encryption, audit logging, and access scoping

Align these controls with applicable regulations:

- GDPR: EU customer data residency, right to erasure, data minimization

- CCPA: California consumer privacy rights, opt-out mechanisms

- FINRA Rule 3310: AML program requirements, SAR reporting, independent testing

- EBA Guidelines: High-risk AI system safeguards for credit scoring

Service and Reasoning Governance

Document and control which agents can interact with which systems (payment APIs, trading platforms, customer onboarding tools) and what actions they can execute.

An orchestrator's reasoning boundaries must:

- Prevent cross-agent interference (one agent cannot modify another agent's data)

- Ensure every action can be traced, justified, and reversed if needed

- Maintain audit logs showing which agent made which decision and why

Regulators and practitioners agree on where the line sits. A Moody's survey found 42% of risk/compliance professionals consider human oversight mandatory, with only 5% comfortable with fully autonomous AI. Build tiered autonomy into every MAS from day one, with human approval gates on high-stakes decisions — not added later as an afterthought.

Security Threat Landscape

OWASP identifies 15 documented threats specific to agentic and multi-agent AI systems:

| Threat | Financial Services Risk | Mitigation |

|---|---|---|

| Memory Poisoning (T1) | Corrupted decision data in trading/lending | Input validation, sanitization of agent memory |

| Tool Misuse (T2) | Agents tricked into unauthorized transactions via prompt injection | Role-based access control, action approval workflows |

| Privilege Compromise (T3) | Weak permissions enabling escalation to sensitive systems | Least-privilege architecture, agent-level permissions |

| Cascading Hallucination (T5) | Misinformation from one agent propagating through entire system | Agent-level explainability tools, confidence thresholds, human checkpoints |

Additional risks include rogue agents exfiltrating financial data, identity spoofing, and agent communication poisoning — where manipulated inter-agent data corrupts compliance workflows before any human reviewer sees it.

The exposure surface is growing fast. AI agent traffic grew 7,851% in 2025, which means every unmitigated threat in the table above now operates at a scale that can cause systemic damage inside a single trading session.

How to Build and Deploy Multi-Agent AI in Finance

Start Narrow

Identify one high-value, well-scoped financial workflow (fraud triage, invoice processing, loan document extraction) as a proof-of-concept before attempting enterprise-wide deployment. Validate that the MAS approach delivers measurable improvement over existing automation before scaling to additional use cases.

Why narrow scope first:

- Faster time to value (weeks vs. months)

- Lower initial investment and risk

- Clear success metrics (processing time, error rate, cost per transaction)

- Easier regulatory approval for limited-scope pilots

Select the Right Tech Stack

Orchestration frameworks:

- LangGraph: Stateful orchestration, human-in-the-loop action approval, multi-agent flows, built-in memory (used by Ally Financial for multi-actor workflows)

- Amazon Bedrock AgentCore: Managed multi-agent orchestration with MCP/A2A protocols

- Microsoft Agent Framework: Successor to AutoGen, enterprise deployment support

LLM providers (choose based on regional compliance):

- OpenAI via Azure: GDPR-compliant deployments, enterprise data residency controls

- Anthropic via AWS: Constitutional AI for safety-critical financial applications

- Google Gemini: Real-time data integration for market analysis use cases

Infrastructure design:

- Hybrid cloud: Sensitive data stays private (on-premise or private cloud), compute-heavy tasks scale on demand (public cloud)

- Containerization: Docker for packaging, Kubernetes for orchestration, ensuring consistent deployment across environments

- Data residency: Ensure EU data stays in EU, US data in US, to comply with GDPR and other regulations

Work with Experienced AI Development Partners

Financial services MAS deployment requires teams that understand both the technical architecture and the regulatory environment. Financial services MAS deployment requires teams that understand both the technical architecture and the regulatory environment.

Gartner reports that 59% of finance leaders use AI (up from 37% in 2023), but 91% report only low or moderate impact during initial stages — most implementations lack the governance depth to deliver transformative results.

Codewave brings hands-on fintech experience across 400+ engagements, with delivery structured around three priorities:

- Maps real financial processes before any agent is built, so design reflects how work actually flows

- Embeds audit trails, access controls, and regulatory safeguards into architecture from day one

- Validates ROI through narrow proof-of-concepts before committing to enterprise-wide rollout

Frequently Asked Questions

What is the best AI for financial services?

There is no single "best" AI—the right choice depends on workflow complexity. RAG models suit simple query tasks like document search and FAQs, while multi-agent AI systems are best for complex, regulated, multi-step workflows across departments like underwriting, fraud detection, and compliance where multiple specialized models must collaborate.

How can agentic AI be used in finance?

Agentic AI acts autonomously on tasks rather than just generating information. Core finance applications include fraud detection, loan processing, insurance claims (FNOL through settlement), portfolio rebalancing, AML/KYC compliance, and intelligent customer service routing—each requiring real-time decision-making across multiple data sources.

What is the difference between single-agent and multi-agent AI in finance?

A single agent handles one isolated task—such as a chatbot answering customer questions. A multi-agent system distributes complex workflows across specialized agents that collaborate: in loan underwriting, for instance, separate agents handle document extraction, credit analysis, fraud detection, and risk modeling under a coordinating orchestrator.

What are the biggest security risks of multi-agent AI in financial services?

Key risks include memory poisoning (corrupting agent decision data), tool misuse (triggering unauthorized transactions), privilege compromise (weak permissions exposing sensitive systems), and cascading hallucinations (false data propagating across agent networks). Strict governance—scoped permissions, service boundaries, and human oversight checkpoints—is the primary defense.

How long does it take to build a multi-agent AI system for a financial institution?

A narrow proof-of-concept can be delivered in weeks with the right partner and a well-scoped workflow (fraud triage, invoice processing). Enterprise-grade deployment with full governance, compliance integration, and cross-system orchestration typically takes several months, depending on complexity, regulatory requirements, and existing infrastructure readiness.