Introduction

Retail banks process hundreds of thousands of customer interactions, loan applications, compliance checks, and account transactions daily, most still relying on manual, error-prone workflows that slow service and inflate costs. A 2024 LexisNexis study found that U.S. and Canadian financial institutions spend $61 billion annually on financial crime compliance alone, with 99% reporting cost increases year-over-year.

The customer side isn't better: 47% of prospective customers globally abandon account applications midway through onboarding due to friction and delays.

RPA (Robotic Process Automation) offers retail banks a way to automate high-volume, rule-based processes without replacing core systems—a pragmatic first step toward digital transformation. This guide covers which workflows qualify for automation, what outcomes banks can realistically expect, and how to build an implementation strategy that delivers measurable results.

Key Takeaways

- RPA automates repetitive, rule-based tasks across customer-facing and back-office banking functions

- Top use cases span customer onboarding, KYC verification, fraud detection, loan processing, and compliance reporting

- Done right, RPA cuts processing time, operational costs, and error rates — often dramatically

- Success depends on choosing the right processes first, not just the right platform

Why Retail Banking Is Uniquely Suited for RPA

Retail banking presents ideal conditions for RPA: enormous transaction volumes, rule-based decision logic, multi-system data dependencies, and low tolerance for errors. These are exactly the conditions where bots outperform humans at scale.

According to Forrester research, financial institutions spend 60-80% of their employees' time on manual, repetitive tasks—work that follows predictable patterns and could be automated. The volume dimension matters: U.S. general-purpose card payments alone reached 153.3 billion transactions in 2022, each requiring verification, processing, and reconciliation across multiple systems.

The legacy system constraint sharpens the case further. 43% of banking systems in the United States are built on COBOL, according to Reuters research. The average age of core banking systems is 20-30 years, and only 8% of banks have modernized their core infrastructure in the past five years.

RPA's non-invasive integration model lets banks automate without overhauling underlying systems — addressing the immediate efficiency problem while allowing longer-term modernization to proceed in parallel.

That combination of volume, legacy debt, and clear ROI has driven rapid market growth. The global RPA in BFSI market was valued at $685.7 million in 2022 and is projected to reach $8.79 billion by 2030 — a 39.4% CAGR — with banking accounting for nearly 60% of adoption.

These conditions don't apply equally across all industries. Retail banking's specific mix of high transaction frequency, strict compliance requirements, and aging infrastructure makes it one of the most automation-ready sectors in financial services:

- Transaction scale: Billions of card payments, account updates, and loan actions processed annually — each requiring multi-system reconciliation

- Rule-based logic: Most processing decisions follow deterministic rules, making them directly automatable without AI judgment

- Compliance pressure: Regulatory reporting demands consistent, auditable workflows — exactly what bots deliver

- Legacy constraints: COBOL-era core systems can't be easily replaced, but RPA layers automation on top without touching the underlying architecture

Customer-Facing Workflows Banks Are Automating with RPA

Customer-facing workflows are high-stakes because they directly affect satisfaction, churn, and onboarding speed—and many are still bottlenecked by manual verification steps across disconnected systems.

Automated Customer Onboarding and KYC

RPA bots extract customer data from submitted documents, cross-reference it against government databases and internal records, validate identity per KYC/AML requirements, and populate account setup fields, cutting onboarding from weeks to hours.

The costs of staying manual are steep. Banks with $10+ billion in assets spend an average of $50 million per year on KYC compliance. Slow onboarding makes that cost worse: 67% of banks globally lost clients due to inefficient onboarding in 2024, and 47% of applicants abandon the process before completing it.

Compliance benefits compound the ROI as well. RPA creates a consistent, auditable record of every onboarding step, reducing regulatory risk and eliminating manual compliance sign-offs. State Street Bank cut the time from account opening to trading by 49% using RPA for KYC processing, generating $1–$2 million in additional revenue per customer through earlier trading access.

Credit Card and Loan Application Processing

For loan and credit card applications, bots access credit bureaus, employment databases, and internal scoring systems simultaneously. They validate applicant information, apply rule-based eligibility logic, and generate approval or escalation decisions, compressing timelines from days to minutes.

For banks processing hundreds of applications per week, the efficiency gain compounds significantly. HDFC Bank reduced turnaround time for loan applications from 40 minutes to 20 minutes, a 50% reduction, while processing approximately 5 million applications per year, achieving 100% error-free data processing across 15+ automated business processes.

Customer Service Query Automation

RPA handles high-frequency, low-complexity queries (balance inquiries, transaction history, account status, application updates) by pulling data from core systems and responding in real time, without human agent involvement.

The handoff model matters: RPA handles the routine volume; human agents are freed for relationship-sensitive or complex escalations, improving both efficiency and customer experience quality. This division of labor allows banks to scale service capacity without proportional headcount increases.

Back-Office Banking Workflows That RPA Handles at Scale

Back-office workflows are where the highest transaction volumes accumulate invisibly: compliance checks, ledger reconciliation, fraud monitoring. Automation ROI here tends to be fastest because there's no customer experience variable to manage.

Fraud Detection and Transaction Monitoring

Manual fraud monitoring simply can't keep pace with real-time transaction volumes. RPA bots handle the full screening cycle:

- Scan transaction data against pre-set rules and behavioral baselines

- Flag anomalies and cross-check against external fraud databases

- Generate alerts or case reports for human review

- Log all actions for audit purposes

The cost of inaction is steep. UK fraud losses reached £1.17 billion in 2024, while the FBI's Internet Crime Report recorded losses exceeding $16 billion in the U.S. alone. Banking and financial services experience more occupational fraud cases than any other industry, with a median loss of $120,000 per case.

RPA doesn't replace fraud analysts. It amplifies their effectiveness by absorbing high-volume screening work and escalating only genuine anomalies for human judgment.

Regulatory Compliance and Reporting

Compliance teams spend significant hours on data gathering and manual entry that RPA can absorb entirely. Bots aggregate data from internal systems, government sources, and regulatory portals, format it per reporting requirements, and submit or store it on schedule. Bot action logs also function as built-in audit trails, addressing a core regulatory requirement.

The cost savings are substantial. Financial institutions spend an estimated 6–10% of revenue on compliance operations. KPMG's 2025 SOX survey puts average compliance budgets at $2.3 million and 15,581 hours annually — time and spend that automation can meaningfully reduce.

Accounts Payable and General Ledger Reconciliation

Month-end bottlenecks in AP typically trace back to the same manual steps: invoice capture, vendor data validation, payment processing, and general ledger updates across disconnected systems. RPA automates the full cycle, often paired with OCR for document capture, eliminating the reconciliation delays that slow finance teams.

The average AP organization takes 9.2 days to process a single invoice at a cost of $9.40 (all-inclusive). Best-in-class organizations process at $2.78 per invoice in 3.1 days: 80% lower cost, 82% faster cycle. That gap is almost entirely explained by how much manual data entry, validation, and routing RPA can absorb.

Direct Debit and Payment Exception Management

Rejected direct debits and payment exceptions follow predictable logic — which makes them ideal for automation. RPA handles the full exception workflow:

- Checks account balances automatically

- Applies standardized business rules consistently

- Processes accepted or rejected transactions without delay

- Logs all outcomes for reconciliation and audit

Previously, this consumed hours of daily manual work per team.

With payment volumes projected to exceed 1.1 trillion transactions annually within five years, no manual team can absorb that volume reliably. RPA ensures consistent rule application and immediate processing without human lag.

Quantifiable Benefits of RPA in Retail Banking

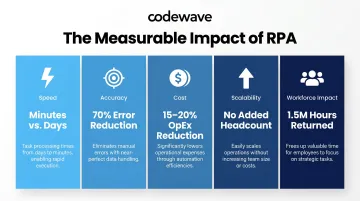

RPA delivers measurable gains across five dimensions that matter to banking operations:

Speed: Tasks completed in minutes vs. days — often completing in seconds what previously took hours. HDFC Bank's 50% reduction in loan processing time and State Street's 49% faster account-to-trading cycle demonstrate real-world velocity gains.

Accuracy: Elimination of data entry errors and inconsistent rule application that create downstream compliance and customer service problems. HDFC Bank achieved 100% error-free data processing, while automation reduced errors for regulatory tasks by 70% according to Gartner research.

Cost: Reduction in FTE hours required for high-volume processing. Best-in-class AP organizations reduce invoice processing costs by 80%, and automation delivers an average 15-20% reduction in recurring operating expenses for banks, per Forrester data.

Scalability: Unlike human teams, RPA bots handle volume spikes — end-of-month processing, application surges — without added headcount or overtime costs. This gives banks a structural edge when managing seasonal or growth-driven demand fluctuations.

Workforce Impact: State Street's automation program returned 1.5 million hours — equivalent to 187,500 workdays — to the business over four years, freeing staff for higher-value work. Deloitte's 2022 survey found 54% of organizations retrained employees for new roles after implementation, making change management as critical as the technology rollout itself.

How to Build a Retail Banking RPA Strategy That Sticks

Step 1: Process Selection

Not every workflow is an RPA candidate. Use a structured assessment framework: score candidate processes on transaction volume, rule-based logic, error sensitivity, and system accessibility.

Start with back-office workflows where ROI is clear and customer impact risk is low—accounts payable, compliance reporting, ledger reconciliation. Then expand to customer-facing use cases like KYC and loan processing after proving the model.

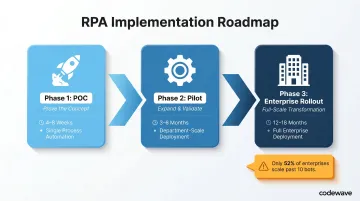

Step 2: Implementation Roadmap

Run a time-bounded proof of concept on one high-volume process before scaling. Define success metrics—error rate, processing time, cost per transaction—upfront.

Common timelines across enterprise RPA deployments follow a predictable arc:

- POC: 4-8 weeks on a single high-volume process

- Pilot: 3-6 months to validate at department scale

- Enterprise rollout: 12-18 months for full deployment

The challenge: only 52% of enterprises progress beyond their first 10 bots. Banks that avoid this stall point treat each phase as a formal gate review—validating ROI before expanding scope rather than scaling prematurely.

Step 3: Governance and Change Management

Establish a centralized RPA governance structure—a Center of Excellence model—to manage bot maintenance, handle system-change impacts, and own ongoing performance monitoring.

Pair this with a change management program that addresses employee concerns and builds internal RPA capability over time. Deloitte found that 34% of workers saw role changes due to automation, making proactive retraining and communication essential for adoption.

Frequently Asked Questions

What does RPA mean in banking?

RPA in banking refers to software bots that mimic human actions to execute repetitive, rule-based tasks across banking systems—such as data entry, document verification, and transaction processing—without manual intervention.

What banking processes are best suited for RPA automation?

Processes with high transaction volume, clear rule-based logic, structured data inputs, and multiple system touchpoints are ideal: KYC verification, loan processing, fraud monitoring, compliance reporting, and accounts payable.

How long does RPA implementation take in retail banking?

A focused proof of concept can be deployed in 4-8 weeks for a single process; enterprise-wide rollout across multiple workflows typically takes 6-18 months depending on complexity and the number of systems involved.

What is the difference between RPA and AI-powered automation in banking?

RPA follows fixed rules and structured workflows, while AI-augmented automation adds machine learning and NLP to handle unstructured data, make judgment-based decisions, and improve over time. Most banks start with RPA, then layer in AI capabilities as their automation maturity grows.

What are the biggest challenges banks face when implementing RPA?

Common challenges include legacy system compatibility, process standardization requirements, change management resistance, and the need for ongoing bot governance as systems evolve. Only 52% of enterprises scale beyond their first 10 bots.

How do banks measure the ROI of RPA investments?

ROI is typically measured through processing time reduction, error rate decline, FTE hours saved, and cost per transaction—with most banks seeing initial ROI within 3-6 months on well-scoped pilot deployments.