Introduction

Insurance is one of the oldest, most risk-averse industries in the world—and right now, it's under pressure from every direction. Policyholders compare their insurer's digital experience to Amazon and digital banks, not other carriers. Insurtech startups are capturing market share with on-demand policies and instant claims.

Meanwhile, legacy core systems that have powered carriers for 20–40 years are buckling under regulatory complexity (GDPR, IFRS 17, state-level data mandates), rising cyber threats, and explosive data volumes. For insurance leaders, the real challenge is no longer whether to transform—it's how to execute without disrupting operations or spending capital on tools that never deliver ROI.

This guide breaks down what digital transformation actually means for insurance companies today: the technologies leading the charge, the measurable outcomes, and a concrete execution roadmap for leaders who need to move.

TLDR:

- Digital transformation spans core systems, customer channels, data infrastructure, and business models—not just digitizing paperwork

- 73% of insurance CEOs prioritize AI investment; 24% cite advancing digitization as their #1 operational focus

- Five pillars must advance together: customer experience, data and analytics, AI/automation, cloud infrastructure, and ecosystem connectivity

- Leading insurers achieve 23-day reductions in claims processing time, 50%+ cost savings in system modernization, and 40% improvements in onboarding efficiency

- Meaningful outcomes emerge in 6–18 months when insurers start with prioritized, high-ROI use cases—even though full transformation takes longer

What Is Digital Transformation in Insurance?

Digital transformation in insurance is the end-to-end integration of technology across operations, products, distribution, and customer experience. It goes far beyond digitizing paperwork — it fundamentally rethinks how insurance value is created and delivered.

This transformation spans multiple layers of the organization:

Core Systems Modernization

Traditional policy administration, claims, and underwriting platforms — many running on mainframe infrastructure from the 1980s and 1990s — are replaced or wrapped with modern API-enabled architectures. A carrier might migrate from a 30-year-old on-premise policy admin system to a cloud-native platform that supports real-time quoting, dynamic pricing, and instant policy issuance.

Customer-Facing Channels

Mobile apps replace paper forms. Self-service portals let policyholders file claims, track status, and update coverage without calling an agent. A P&C insurer, for instance, might deploy an app where customers photograph accident damage, receive an AI-generated estimate in minutes, and approve repairs — no human intervention required.

Data Infrastructure

Insurers consolidate siloed data from underwriting, claims, finance, and distribution into centralized data lakes or cloud warehouses. A health insurer might integrate claims history, electronic health records, and wearable device data to build predictive models that flag high-risk members before costly interventions occur.

New Business Models

Transformation unlocks entirely new revenue streams: embedded insurance (coverage sold at point of purchase in e-commerce checkouts or ride-share apps), usage-based insurance (premiums tied to telematics-captured behavior), and parametric policies (automatic payouts triggered by defined events like earthquake intensity or rainfall levels).

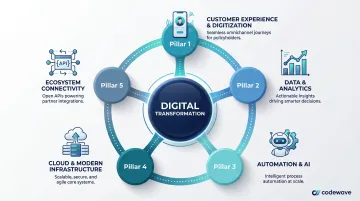

The 5 Pillars of Digital Transformation in Insurance

Lasting transformation requires coordinated progress across five foundational pillars:

- Customer Experience & Digitization – Omnichannel engagement, self-service portals, and mobile-first design that meet policyholder expectations shaped by digital banking and e-commerce

- Data & Analytics – Centralized data infrastructure and predictive modeling that turn unstructured inputs (claims notes, images, sensor feeds) into actionable intelligence

- Automation & AI – Robotic process automation for high-volume tasks, machine learning for underwriting and fraud detection, and NLP for document analysis

- Cloud & Modern Infrastructure – Migration from legacy on-premise systems to cloud platforms that enable real-time processing, API connectivity, and cost efficiency

- Ecosystem Connectivity – API-first architecture that integrates insurtechs, benefit administrators, distribution partners, and third-party data providers into a connected, interoperable network

These pillars are interdependent — automation initiatives fail without clean data; analytics models can't scale without cloud infrastructure; customer experience improvements stall when core systems can't support real-time interactions. The sections below break down exactly how insurers move each pillar forward in practice.

Why Insurance Companies Can No Longer Delay

Competitive Pressure from Insurtechs

The global insurtech market grew from approximately $6.09 billion in 2024 to a projected $23.06 billion by 2032, with P&C insurtech funding rebounding 34.9% in 2025 alone. Digital-native carriers and insurtech startups are gaining ground by offering instant quotes, on-demand policies, and seamless, one-click claims experiences that legacy carriers struggle to match. Meanwhile, 73% of insurance CEOs agree AI is a top investment priority, and 24% cite "advancing digitization and connectivity across the business" as their number-one operational priority—the highest-ranked item in KPMG's 2025 survey of 110 insurance CEOs.

Shifting Policyholder Expectations

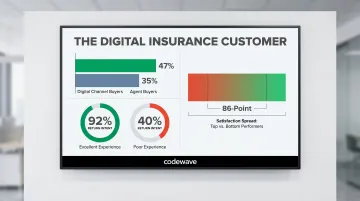

Today's insurance customers no longer compare their carrier's digital experience to other insurers—they compare it to Amazon, Uber, and their digital bank. 57% of auto insurance customers actively shopped for a new policy in 2024, the highest shopping rate JD Power has ever recorded. The underlying numbers explain why that shopping rate matters:

- 47% of shoppers now buy through digital channels vs. 35% through traditional agents

- 86-point satisfaction gap separates top- and bottom-performing insurers on digital quoting (1,000-point scale)

- 92% of customers with excellent digital experiences (score 801+) say they'll definitely return via digital channels

- 40% — the return intent rate for customers with poor experiences (score 500 or below)

That gap between 92% and 40% translates directly into churn and lost acquisition.

Regulatory and Data Pressure

Compliance requirements—GDPR, IFRS 17, state-level data regulations—and the growing volume of unstructured data are exposing the limits of legacy systems. 83% of insurance CEOs cite cybercrime and cyber insecurity as the top trend negatively impacting their business, and 53% name cybersecurity and digital risk resilience as their number-one risk mitigation investment.

IFRS 17—effective since January 2023—continues to challenge insurers worldwide, with the IMF still running implementation workshops for supervisors as recently as 2026. For carriers still on legacy infrastructure, modernization is no longer optional: it's a compliance and operational survival issue.

Core Technologies Driving Insurance Digital Transformation

Five technologies are reshaping how insurers price risk, process claims, and serve customers — and they work best when deployed together, not in isolation.

AI and Machine Learning in Underwriting and Claims

AI-powered models analyze structured and unstructured data—medical records, telematics feeds, claims images, credit history, and even satellite imagery—to automate risk scoring, flag anomalies, and accelerate underwriting from days to minutes. Machine learning-based fraud detection systems reduce false positives compared to legacy rules-based approaches by learning evolving fraud patterns rather than relying on static rules.

UK insurer Aviva deployed 80+ AI models to improve claims outcomes, achieving a 23-day reduction in liability assessment time for complex claims, 30% improvement in routing accuracy, a 65% reduction in customer complaints, and total savings of 60 million GBP (approximately $82 million) in 2024 from its motor claims domain transformation alone.

Yet adoption remains uneven. 41% of insurers are actively using AI across core business areas, and nearly 60% expect AI to significantly transform their business models within 1 to 3 years—but fewer than 20% agree their organization is at an advanced stage of AI implementation.

IoT and Telematics for Usage-Based Insurance

Connected devices—vehicle telematics, wearables, smart home sensors—feed real-time behavioral data into dynamic pricing models. Usage-based insurance (UBI) and parametric insurance represent a fundamental shift: the insurer's role moves from reactive payer to proactive risk partner.

The global insurance telematics market is projected to grow at 18.9% annually through 2034. Already, 87% of commercial fleets use telematics infrastructure, and 60% of insurers deploy telematics across their risk control teams. The impact is measurable: telematics accelerates risk reduction, improving the highest-risk driver scores by 40% within three months. Fleets combining continuous monitoring with targeted driver training achieve a 77% reduction in violations.

Parametric insurance powered by IoT demonstrates transformation's business model potential. Allianz uses satellite rainfall data to automatically trigger payouts when rainfall levels threaten crops, protecting over $1.5 million in investments across 390 hectares and 45 municipalities in Colombia. Similarly, Swiss Re offers parametric products triggered by earthquake shake intensity, tropical cyclone magnitude, and vegetation indices—including a New York City parametric flood cover providing up to $1.1 million in emergency funding for low-to-moderate income communities.

Cloud Migration and Legacy Modernization

Most insurers run on core systems that are 20–40 years old. 74% of insurers continue to rely on outdated legacy systems, and approximately 70% of IT budgets are consumed maintaining this legacy infrastructure—leaving limited capacity for innovation. Compounding the problem: 60% of mainframe technology specialists are nearing retirement age, creating acute talent risk.

Cloud migration is the infrastructure prerequisite for everything else—enabling API connectivity, real-time data processing, omnichannel delivery, and cost-efficient scaling. The cloud services in insurance market is projected to grow at 14.5% annually during 2025-2034.

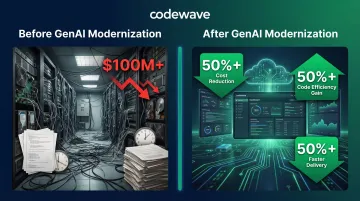

Generative AI is accelerating modernization economics: one top-15 global insurer reduced the cost of modernizing a legacy transaction processing system from over $100 million to less than $50 million—a 50%+ cost reduction—while achieving 50%+ improvements in code modernization efficiency and testing, and 50%+ acceleration in coding task speed.

Robotic Process Automation (RPA) and Workflow Automation

High-volume, rules-based tasks—policy renewals, claims intake, compliance reporting, document verification, invoice processing—are ideal automation candidates. Organizations that moved beyond piloting intelligent automation achieved an average cost reduction of 32%, up from 24% in prior survey waves.

McKinsey estimates insurers may eventually automate 50% to 60% of traditional back-office operations. One global insurer formed interdisciplinary pods that automated nearly 30% of the insurer's manual operations tasks, designing and implementing new processes in one-third the time taken by traditional specialist teams. Digital-first companies can shrink their expense ratios by as much as 40% compared to traditional P&C insurers.

Advanced Analytics and Predictive Modeling

The shift from descriptive reporting (what happened) to predictive analytics (what will happen) and prescriptive analytics (what to do about it) is redefining how insurers manage risk. Actuarial teams now use these models for customer lifetime value scoring, churn prediction, and dynamic pricing—but unstructured data (claims notes, social data, satellite imagery) remains largely untapped by most insurers.

McKinsey estimates 1.2 trillion euros in realized and potential value from analytics globally in the insurance sector. Yet 86% of EMEA insurers realize less than 5% of their operating profit from advanced analytics or don't track value capture at all. None of the 59 surveyed organizations considered themselves analytics-driven.

Top performers move from exploration to rollout in less than 3 months; average insurers take 9 to 12 months per use case. The payoff is significant: top performers realized 10% to 25% uplift in operating profit from analytics, with some expecting over 25% in the following two years.

The Business Case: What Digital Transformation Delivers

Operational Benefits

Digital transformation delivers faster processing cycles, lower cost ratios, reduced manual error, and improved fraud detection. Codewave has helped financial and insurance clients achieve measurable outcomes across engagements:

- 50% faster invoice processing

- 99% reduction in fraud risk exposure

- 40% gain in team productivity

At the industry level, McKinsey research shows domain-level AI rewiring can deliver 20–40% reductions in customer onboarding costs, 10–20% improvements in new-agent sales conversion, and 3–5% gains in claims accuracy.

Customer Experience Benefits

Personalized policy recommendations, self-service portals, real-time claims tracking, and omnichannel engagement drive policyholder satisfaction and retention. The numbers from recent carrier transformations reflect how quickly these gains compound:

- One insurer moved 80% of transactions online after automating quotes and sales

- A 24/7 after-hours chatbot produced an 11% increase in policy purchases from prospective customers

- A sales automation rollout at a separate carrier produced a 36-percentage-point jump in customer satisfaction scores (likelihood to refer)

Strategic Value

Digital transformation extends well beyond operational efficiency — it opens revenue streams that legacy infrastructure simply cannot reach. Embedded insurance (coverage sold within ride-share apps, e-commerce checkouts, or digital wallets), microinsurance, and ecosystem plays represent growth opportunities that require modern infrastructure and API connectivity.

Over the past five years, insurance-sector AI leaders created 6.1 times the total shareholder return (TSR) of AI laggards—a multiple two to three times higher than in most other sectors.

How to Execute Digital Transformation in Insurance: A Practical Roadmap

The biggest execution failures happen when insurers treat transformation as a one-time IT initiative rather than an ongoing business strategy with technology as the enabler. A phased approach keeps investments grounded in real outcomes and builds momentum across the organization.

Phase 1: Define Outcomes Before Choosing Technology

Establish measurable business outcomes—reduce claims processing time by X%, improve NPS by Y points, cut fraud losses by Z%—before evaluating technology. This outcome-first approach ensures transformation investments are tied to real business value, not just tool adoption.

Ask: What specific business problem are we solving? How will we measure success? What does a 10% improvement in this metric mean in dollar terms?

Phase 2: Audit Legacy Infrastructure and Data Maturity

Conduct a technology and data audit: map current system architecture, identify integration constraints, assess data quality and accessibility across silos. This diagnostic phase surfaces the technical debt that must be addressed before new capabilities can be layered on.

Document:

- Which core systems handle policy admin, claims, underwriting, and billing

- Where data lives and how it flows between systems

- Data quality issues (completeness, accuracy, consistency)

- Integration points and API availability

- Talent gaps and technical skills needed

Phase 3: Prioritize Use Cases with the Highest ROI

Identify 3–5 transformation use cases where the business pain is highest and the technology solution is proven—such as claims automation, fraud detection, or digital self-service. Sequencing matters: early wins build organizational confidence, fund further investment, and demonstrate ROI to skeptical stakeholders.

Common high-ROI insurance use cases include:

- Claims automation – Reducing manual intake, routing, and settlement time

- Fraud detection – Applying ML models to flag suspicious patterns in claims data

- Digital self-service – Enabling policyholders to manage accounts, file claims, and update coverage online

- Underwriting automation – Accelerating risk assessment using AI-powered data analysis

- Policy renewal automation – Accelerating renewals with predictive analytics and automated outreach

Phase 4: Build for Ecosystem Connectivity, Not Point Solutions

Digital transformation in insurance requires an API-first architecture that enables integration with insurtechs, HRIS platforms, benefit administrators, distribution partners, and regulators. Building isolated point solutions creates new silos.

The goal is a network of interconnected stakeholders where data flows freely across the value chain. A commercial auto insurer, for instance, should be able to ingest telematics data from fleet management platforms, share risk scores with brokers via API, and automatically update policy terms based on driver behavior. No manual intervention required.

Avoid the temptation to build custom integrations for every partner. Instead, invest in middleware platforms or API gateways that provide reusable connectivity across partners.

Phase 5: Measure, Iterate, and Scale

Transformation doesn't end at go-live. Set leading and lagging KPIs, run adoption assessments, collect employee and customer feedback, and use those inputs to iterate on rollout strategy.

Leading indicators:

- User adoption rates (employees and customers)

- Process completion rates

- Time-to-value metrics (time from quote to policy issuance, claim filing to settlement)

Lagging indicators:

- Claims processing speed

- Cost per policy

- Fraud loss ratio

- Net Promoter Score (NPS)

- Customer retention rate

Agile delivery—validated incrementally, not launched in a big-bang release—reduces risk and accelerates time-to-value. A practical rule of thumb: plan to invest as much on user adoption and scaling as on the development itself. Without deliberate change management, even well-built solutions underdeliver.

Key Challenges and How to Navigate Them

Legacy System Integration

The most common execution blocker is the technical complexity of connecting new tools to decades-old core systems. Rather than high-risk, high-cost rip-and-replace projects, consider phased modernization approaches: wrap legacy systems with APIs before full replacement, migrate one module at a time (e.g., claims before policy admin), or run new and old systems in parallel during transition periods.

Cultural Resistance and Change Fatigue

Mid-level managers and frontline employees are statistically the most likely to resist digital change. BCG research shows that 74% of corporate transformations fail to create both short- and long-term value, often due to change management failures. Transformation succeeds when people understand the "why," receive role-specific training, and see leaders actively model new behaviors—not just when new software is deployed.

The data reinforces this. According to KPMG's US Insurance CEO report:

- 29% of insurance CEOs cite "employee reluctance or ability to adapt" as a top AI implementation challenge

- 77% identify AI workforce readiness and upskilling as a constraint on growth

- Change management accounts for 50% of the effort required for transformation impact — equal to data modeling and integration combined

Data Quality and Governance

AI models are only as reliable as the data they're trained on. 51% of insurance CEOs cite "data readiness" as a top challenge in implementing AI, and 56% of non-top-performing insurers cite data as a top-five roadblock to analytics adoption.

Establish data governance standards and ownership accountability before investing in advanced analytics infrastructure. Practical starting points include:

- Defining authoritative data sources for key metrics across business units

- Implementing validation checks that flag inconsistencies at ingestion

- Mapping data lineage so teams understand where data originates and how it changes

Frequently Asked Questions

What is the digital transformation of the insurance industry?

Digital transformation in insurance is the process of integrating technologies like AI, cloud computing, automation, and data analytics across operations, products, and customer touchpoints to modernize how insurers assess risk, process claims, and deliver policyholder experiences. It goes beyond digitizing paperwork — it changes how insurers create products, price risk, and serve customers.

What are the 5 pillars of digital transformation?

The five pillars are: customer experience and digitization, data and analytics, AI and automation, cloud and modern infrastructure, and ecosystem connectivity. Lasting transformation requires progress across all five — not just one or two, since each pillar depends on the others to deliver results.

What technologies are most critical for digital transformation in insurance?

AI/ML for underwriting and fraud detection, cloud platforms for scalability and cost efficiency, IoT/telematics for usage-based products, RPA for process automation, and advanced analytics for risk modeling and customer intelligence.

What are the biggest barriers to digital transformation in insurance?

Legacy system debt, organizational resistance to change, poor data quality, and lack of a clear outcome-driven strategy are the most common barriers. Most failures trace back to people and process, not technology — 74% of corporate transformations fail to create lasting value because change management was underinvested or outcomes weren't defined before technology was purchased.

How long does digital transformation take for an insurance company?

Full transformation is a multi-year journey, but meaningful outcomes — automated claims, digital self-service, fraud detection — can be realized within 6–18 months by starting with high-ROI use cases. Top performers move from exploration to rollout in under 3 months per use case; average insurers take 9–12 months.

How do insurers measure the success of digital transformation?

Use a mix of operational KPIs (claims processing speed, cost per policy, fraud loss ratio), customer metrics (NPS, self-service adoption, retention rate), and adoption metrics (employee utilization of new tools). Measurement should be defined before transformation begins, not after. For every $1 spent on building solutions, plan to spend at least $1 on user adoption and scaling.